![]() Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

Chicago, Illinois

Chicago Apartment Loans in 2026

Select Commercial specializes in Chicago apartment loan solutions for local investors, plus apartment building financing for larger properties and portfolios, with rates as low as 6.16% and up to 80% LTV. For properties elsewhere in the state, see our Illinois apartment loans; for loans over $6 million, see Chicago multifamily loans. See current rates on every loan type we offer.

Get a Free QuoteFinancing Options in Chicago

Chicago apartment, multifamily and commercial properties each have dedicated financing. Pick the page that matches your property:

Financing more of the state? See Illinois apartment loans and Illinois commercial mortgages.

Financing in another state? Explore our apartment loans, multifamily loans and commercial mortgages nationwide.

Chicago Apartment Loan Rates (Under $6 Million)

| Loan Type | Rate* | Max LTV |

|---|---|---|

| Apartment 5 Year Fixed | 6.16% | Up to 80% |

| Apartment 7 Year Fixed | 6.14% | Up to 80% |

| Apartment 10 Year Fixed | 6.16% | Up to 80% |

- Rates as low as 6.16% on Chicago apartment loans

- Up to 80% LTV on apartment financing

- Terms and amortizations up to 30 years

- Purchase and refinance, including cash-out

- No upfront application or processing fees

- 48-hour written pre-approvals, no cost or obligation

Rates last updated August 8, 2026. Rates and maximum LTV shown represent our best-case pricing scenarios. Actual rates, LTV, and loan terms are subject to underwriting approval and may vary.

Compare Chicago Apartment Loan Programs

As a broker, we compare every program to find your best-fit Chicago apartment financing. Typical starting points for properties under $6 million:

| Program | Typical rate* | Max leverage | Best for |

|---|---|---|---|

| Fannie Mae Small Loan | 6.16%-6.95% | Up to 80% | Non-recourse, fixed to 30 yrs |

| Freddie Mac SBL | 6.15% | Up to 80% | $1M to $7.5M small balance |

| FHA / HUD | 6.12% | Up to 85% | Highest leverage, longest term |

| Bank / portfolio | 6.25%-6.50% | Up to 75% | Flexible, value-add |

| Bridge | 9.00% | Up to 80% LTC | Reposition, lease-up |

Most apartment lenders look for a debt-service-coverage ratio (DSCR) of at least 1.25x. Chicago’s strong occupancy and rent growth help many buildings clear that threshold comfortably. For properties over $6 million, see our Chicago multifamily loans.

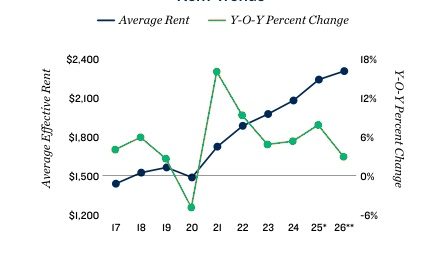

2026 Chicago Apartment Loan Market: Tight Vacancy Supports a Stable Outlook

Chicago enters 2026 with a narrow development pipeline and vacancy that remains historically tight. Investors pursuing apartment building loans focus on the same fundamentals that shape a Chicago apartment loan: job growth, the pace of deliveries, vacancy direction and rent momentum.

Employment outlook remains positive

Total employment is projected to expand by about 13,000 jobs in 2026. That pace is below the metro’s long-term average but still faster than the national pace.

Construction stays limited

Completions in 2026 are projected to expand inventory by about 0.5%, among the smallest increases nationwide. Deliveries are expected to fall below 4,000 units for the first time since 2012, with a forecast of roughly 3,900 units.

Vacancy stays tight

Slower hiring is expected to push vacancy slightly higher, but the year-end rate is forecast around 3.8%, still about 200 basis points below the metro’s long-term average.

Rent growth moderates

With vacancy edging higher, rent growth slows after a strong five-year run. The year-end mean rent is projected near $2,300 per month, with rent growth around 2.9%.

2026 Chicago forecast at a glance:

- Employment: about 13,000 new jobs

- Construction: about 0.5% inventory growth, roughly 3,900 units

- Vacancy: up about 20 bps to roughly 3.8%

- Rent: about +2.9%, mean near $2,300 per month

Limited construction and low vacancy keep Chicago near the top of major-market rankings. For investors evaluating apartment building loans, these trends support underwriting assumptions and strengthen the case for a Chicago apartment loan tied to stable occupancy and durable rents.

Chicago Multifamily Loans (Over $6 Million)

For larger Chicago apartment properties, we arrange multifamily loans over $6 million through Fannie Mae DUS, Freddie Mac, FHA/HUD and CMBS. These institutional programs offer non-recourse financing, up to 80% LTV and fixed terms up to 30 years, with even longer, fully amortizing options through HUD. Chicago’s tight vacancy and durable rents make large, stabilized multifamily assets attractive to agency lenders, which often translates into the tightest available pricing.

Whether you are financing a downtown high-rise, a lakefront elevator building or a large suburban garden community, we compare every large-balance option. See our Chicago multifamily loans page for over-$6 million financing, or Fannie Mae and Freddie Mac for agency programs.

Recent Apartment Loan Closings

A sample of apartment and multifamily loans we have arranged for investors nationwide.

Chicago Neighborhoods & Submarkets We Finance

We finance apartment and multifamily properties across the city’s neighborhoods and submarkets, from high-rise corridors downtown to established rental communities on the North and South Sides, including:

- The Loop

- River North

- West Loop

- South Loop

- Streeterville

- Gold Coast

- Lincoln Park

- Lakeview

- Wicker Park

- Logan Square

- Hyde Park

- Pilsen

- Uptown

- Rogers Park

- Bronzeville

- Albany Park

- Edgewater

- Andersonville

Chicago Apartment Loan Types We Serve

Whether you are purchasing or refinancing a Chicago apartment building, we arrange financing for:

- Large urban high-rise apartment buildings

- Suburban garden apartment complexes

- Small apartment buildings with 5+ units

- Underlying cooperative apartment loans

- Portfolios of small apartment and single-family rental properties

- Other multifamily and mixed-use properties

We consider apartment loan requests of all sizes, beginning at $1,500,000.

Loan Programs for Chicago Apartments

As a broker, we compare every program to find your best-fit Chicago apartment financing:

Fannie Mae

Small Loan and DUS programs, non-recourse, fixed up to 30 years.

Freddie Mac SBL

$2M to $10M, streamlined small-balance multifamily.

FHA / HUD

Highest leverage and longest fully amortizing terms.

Bank / Portfolio

Flexible financing for value-add and non-standard deals.

For properties over $6 million, see our Chicago multifamily loans. For other cities in the state, see Illinois apartment loans.

Other Property & Loan Types We Finance in Chicago

As a full-service commercial mortgage broker, we arrange Chicago financing across every major property and loan type:

We consider commercial loan requests of all sizes, beginning at $1,500,000.

Chicago Areas We Serve

Select Commercial provides apartment loans throughout Chicago, Illinois and the surrounding suburbs, including:

- Addison

- Algonquin

- Arlington Heights

- Aurora

- Barrington

- Bartlett

- Batavia

- Bolingbrook

- Buffalo Grove

- Carol Stream

- Des Plaines

- Downers Grove

- Elgin

- Elmhurst

- Glen Ellyn

- Glenview

- Gurnee

- Hanover Park

- Highland Park

- Hinsdale

- Joliet

- Lake Forest

- Lombard

- Morton Grove

- Mundelein

- Naperville

- Northbrook

- Oak Brook

- Oak Lawn

- Oak Park

- Orland Park

- Rolling Meadows

- Round Lake Beach

- Schaumburg

- St. Charles

- Tinley Park

- Waukegan

- Westmont

- Wheaton

- Wheeling

What Our Clients Say

“I am a veterinarian who purchased an existing practice. I was surprised to find a company that offered 100% financing at a good rate, with great terms and rates for medical office financing.”

Carol K. · Chicago, IL“I spoke to several commercial lenders before finding Select Commercial. They got me a lower rate and their service was exceptional. If you need a multifamily loan, you need to talk to Stephen.”

Nathan B. · Philadelphia, PA“Select Commercial was very helpful with my multifamily mortgage. Stephen went over several options and we came up with the best lender to meet my needs. I got the funds and also lowered my payments.”

Gary M. · Portland, OR“Select Commercial offered 100% financing for my medical practice when my bank would have required 20% down. They delivered something my bank could not, and handled everything professionally.”

John C. · Boston, MAGet Your Chicago Apartment Loan Quote

No cost, no obligation. Written answers within 48 hours on Chicago apartment loans from $1,500,000.

- No application or processing fees

- Written answers within 48 hours

- For 5+ unit and commercial properties, $1.5M and up