Minnesota Apartment Loan Rates

Select Commercial offers some of the most competitive Minnesota apartment loan rates available, with 5, 7, and 10-year fixed-rate options starting as low as 5.90% as of July 5, 2026. As one of the most experienced apartment lenders in Minnesota, we arrange apartment building loans and apartment building financing for properties valued between $1.5 million and $6 million, with up to 80% LTV, 30-year amortizations, and no upfront fees. For loans over $6 million, see our Minnesota multifamily loan options.

| MN Apartment Loan Rates Less Than $6 Million | Free Loan Quote | ||

|---|---|---|---|

| Loan Type | Rate* | LTV | |

| Apartment Loan 5 Yr Fixed | 5.90% | Up to 80% | |

| Apartment Loan 7 Yr Fixed | 5.86% | Up to 80% | |

| Apartment Loan 10 Yr Fixed | 5.85% | Up to 80% | |

| MN Multifamily Loan Rates More Than $6 Million | Free Loan Quote | ||

|---|---|---|---|

| Loan Type | Rate* | LTV | |

| Multifamily Loan 5 Yr Fixed | 5.50% | Up to 75% | |

| Multifamily Loan 7 Yr Fixed | 5.46% | Up to 75% | |

| Multifamily Loan 10 Yr Fixed | 5.45% | Up to 75% | |

*Rates start as low as the rates stated here. Your rate, LTV, and amortization will be determined by underwriting.

Minnesota apartment loan rates are priced based on the U.S. Treasury yield curve. As of July 5, 2026, the 10-year Treasury yield is 4.487% and the 5-year Treasury yield is 4.221%, which directly influences current pricing on apartment building loans in Minnesota.

Want a personalized quote? Click here to request a customized loan quote for your Minnesota apartment property.

Why Select Commercial Offers Competitive Minnesota Apartment Loan Rates

When investors search for the best apartment loan rates in Minnesota, Select Commercial consistently delivers some of the most competitive pricing available for properties under $6 million. We work directly with Fannie Mae Small Loan, Freddie Mac SBL, CMBS conduits, life insurance companies, banks, and credit unions, which means borrowers gain access to a wide network of apartment lenders in Minnesota rather than the rates of a single bank. This multi-source approach allows us to consistently match borrowers with the lowest available rate and best terms for their specific apartment property.

Our Minnesota apartment building financing programs include 5, 7, and 10-year fixed-rate options, up to 80% LTV, 30-year amortizations, non-recourse availability, and no upfront fees. Whether you are acquiring, refinancing, or pulling cash out of a stabilized apartment property valued between $1.5 million and $6 million, our team structures apartment building loans tailored to your investment goals.

Need a multifamily loan over $6 million? Visit our Minnesota multifamily loan page. For other commercial property types, explore our Minnesota commercial mortgage options. To compare all rates nationwide, see commercial mortgage rates.

2026 Minnesota Apartment Loan Market Overview

Entering 2026, Minnesota presents a stable and institutionally supported apartment market anchored by the Minneapolis–St. Paul metro. For borrowers evaluating apartment loans, the state benefits from diversified employment across healthcare, finance, and corporate headquarters, combined with steady renter demand and relatively balanced supply conditions. This environment supports apartment building financing focused on consistent occupancy, durable rent collections, and long-term asset performance.

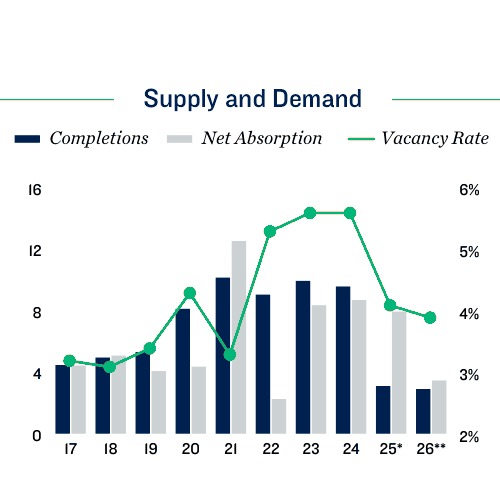

Development activity across Minnesota has remained active but controlled, with new supply largely concentrated in the Twin Cities. Absorption has generally kept pace with deliveries, helping maintain manageable vacancy levels. For apartment lenders, Minnesota provides an underwriting environment centered on stability, tenant quality, and long-term income rather than aggressive rent growth assumptions.

Minneapolis Anchors Minnesota Apartment Loans

Minneapolis remains the primary driver of apartment activity across Minnesota. In 2026, the metro is projected to add approximately 18,000 jobs, deliver roughly 6,000 units, maintain vacancy near 5.7%, and reach average effective rent around $1,600 per month. For borrowers seeking an apartment building loan, Minneapolis offers institutional scale, diversified employment, and consistent renter demand.

Saint Paul Provides Stability and Government-Driven Demand

Saint Paul complements Minneapolis with a stable apartment market supported by government, healthcare, and education employment. The city has a population of approximately 310,000, median household income near $65,000, median rent around $1,450, and median home value near $320,000. These fundamentals support steady occupancy and reliable rent performance.

Rochester Adds Healthcare-Driven Growth

Rochester provides a strong secondary apartment market driven by healthcare employment and regional growth. The city has a population of approximately 120,000, median household income near $80,000, median rent around $1,500, and median home value near $360,000. This supports consistent renter demand and long-term investment stability.

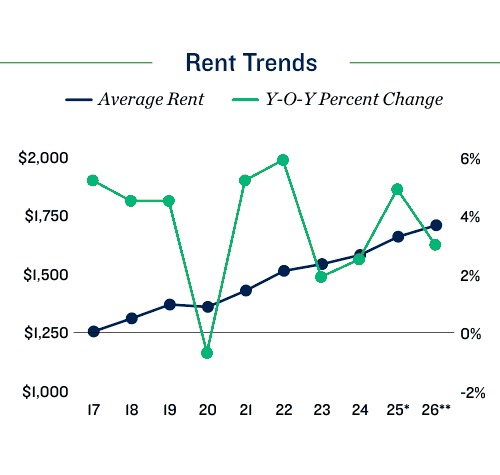

Rent Levels Reflect Stability Across the Twin Cities

Minnesota maintains a balanced rent profile relative to national averages. Minneapolis is projected near $1,600 per month, with Saint Paul and Rochester slightly below or near that range. This allows borrowers to structure apartment loans across both urban and secondary markets with consistent demand characteristics.

2026 Minnesota Apartment Loan Market Forecast

- Employment: Minneapolis is projected to add approximately 18,000 jobs.

- Construction: Minneapolis is projected to deliver roughly 6,000 units.

- Vacancy: Vacancy is projected near 5.7%.

- Rent: Average effective rent is projected near $1,600 per month.

For investors comparing apartment loans in Minnesota, 2026 reflects a market centered on stability and diversification. Minneapolis provides the primary scale and liquidity, while Saint Paul and Rochester offer complementary opportunities supported by government and healthcare employment.

2026 Minneapolis Minnesota Apartment Loan Market Overview

Minneapolis is Minnesota's largest city and the primary driver of apartment loans in Minnesota, anchoring the state's most active rental investment market as the economic hub of the Upper Midwest. The city has a population of approximately 427,499 residents as of 2026, with a median household income of approximately $80,846, up approximately 5.16% year-over-year in 2023, and a median property value of approximately $345,600 as of 2023. Approximately 100,754 renter-occupied households represent approximately 52% of all occupied housing units. Current data points to an average apartment rent of approximately $1,689 per month as of March 23, 2026, up 1.99% year-over-year, and a median rent approximately 13% below the national average, reflecting the city's relative affordability compared to other major metros of similar economic scale. Minneapolis ranks approximately 23rd nationally for employment strength in 2026 and is home to the headquarters of Minnesota's 15 Fortune 500 companies, including UnitedHealth Group and Target, supporting one of the most diversified and recession-resilient employment bases among Midwest cities. These fundamentals continue to support consistent demand for Minnesota apartment loans across the Twin Cities metro.

Minneapolis Minnesota Apartment Loan Rates and Financing in 2026

Financing conditions for Minnesota apartment loans remain active in Minneapolis in 2026, with lenders supporting stabilized assets across all classes, newer Class A communities in suburban growth corridors, and value-add acquisitions in the city's large pre-war and mid-century urban rental stock. The median property value of approximately $345,600 reflects a market where homeownership costs are meaningful but the city's 52% renter-occupied rate indicates a structural preference for renting among a broad professional renter base. The suburban submarkets of Eden Prairie and Edina maintain approximately 93.8% and 94.3% occupancy respectively heading into 2026, and the Northeast Minneapolis submarket projects approximately 95.8% occupancy, among the strongest readings in the Twin Cities metro. For borrowers seeking an apartment building loan in Minneapolis, the city's diversified Fortune 500 employment base, improving submarket occupancy, and a sharp slowdown in new supply are expected to support tightening vacancy heading into 2026 within the broader Minnesota apartment building financing landscape.

Trends in the Minneapolis Minnesota Apartment Market

Minneapolis' rental market benefits from the most diversified Fortune 500 employment concentration of any Upper Midwest city. Healthcare and social assistance leads at approximately 35,535 workers, anchored by UnitedHealth Group, Fairview Health Services, and Allina Health; educational services at approximately 29,828 workers, anchored by the University of Minnesota-Twin Cities, which awarded approximately 13,676 degrees in 2022; and professional, scientific, and technical services at approximately 29,573 workers. Finance and insurance pays the highest median earnings at approximately $94,242, reflecting the presence of U.S. Bancorp, Ameriprise Financial, and dozens of regional financial institutions. Minneapolis ranks 23rd nationally for employment strength in 2026, and the tech sector is expanding with companies such as NetSPI establishing headquarters locally. The city's median age of approximately 33.4 years reflects a young, professionally driven renter demographic, and renters in the 25 to 34 age group make up the largest cohort at 37%. These fundamentals continue to attract Minnesota apartment lenders evaluating the state's primary market.

Minneapolis Minnesota Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Minneapolis is approximately $1,689 per month, up 1.99% from $1,656 the prior year, and the median rent is approximately $1,651 per month, approximately 13% below the national average. By unit type: studios average approximately $1,205/month, one-bedrooms average approximately $1,504/month, two-bedrooms average approximately $2,078/month, and three-bedrooms average approximately $2,441/month. Approximately 39% of all Minneapolis rentals are priced between $1,001 and $1,500 per month, reflecting a predominantly workforce and professional mid-tier rental base. The Cedar-Isles-Dean neighborhood commands the highest rents at approximately $2,564/month, while Northeast Minneapolis and Uptown remain the most active investment submarkets. These rent levels support consistent underwriting for apartment loans in Minnesota where Fortune 500 employment and a high-income renter base anchor stable occupancy.

Minneapolis Minnesota Apartment Loan Supply and Demand in 2026

Minneapolis is entering 2026 with improving supply-demand conditions as a sharp slowdown in new supply deliveries is expected to tighten vacancy across most suburban submarkets. The downtown Minneapolis occupancy was approximately 92.1% as of Q4 2025 projections, lagging the metro-wide average, while suburban submarkets such as Northeast Minneapolis project approximately 95.8% occupancy and Highland/Macalester-Groveland/Summit Hill approximately 95.3%. Approximately 30% of Minneapolis' rental stock was built before 1939, and newer inventory built between 2010 and 2019 represents approximately 13% of all units, a reflection of the city's sustained post-recession development cycle. One-bedroom units make up the largest share of rental inventory at approximately 41% of all units, consistent with the market's young professional and single-person renter orientation. For borrowers pursuing apartment building financing in Minnesota, the city's improving vacancy trajectory, declining new supply pipeline, and robust suburban submarket occupancy support a favorable long-term underwriting environment.

Opportunities for Apartment Investment in Minneapolis Minnesota

Investors pursuing a Minnesota apartment loan in Minneapolis in 2026 are focused on long-term income stability in diversified tenant submarkets near major corporate campuses and healthcare corridors, value-add acquisitions in the city's large pre-war and 1970s vintage rental stock, and stabilized holds in high-occupancy suburban submarkets such as Northeast Minneapolis, Uptown, and the southwest corridor where demand from young professionals and corporate employees is most concentrated. Minneapolis' median household income of approximately $80,846 grew approximately 5.16% year-over-year in 2023, supporting consistent renter income capacity and rent growth potential. The city's average commute of approximately 23 minutes and extensive public transit network including light rail lines reinforce quality-of-life appeal for urban renters. For Minnesota apartment lenders evaluating the state's primary market, Minneapolis offers the most diversified Fortune 500 employment base in the Upper Midwest, a high-income renter demographic, and a tightening supply-demand balance that supports strong long-term performance for apartment building loans throughout the metro.

2026 Saint Paul Minnesota Apartment Loan Market Overview

Saint Paul is Minnesota's capital city and second-largest market for apartment loans in Minnesota, anchored by state government, healthcare, manufacturing, and university employment and offering relative affordability within the Twin Cities metro. The city has a population of approximately 305,634 residents as of 2026, with a median household income of approximately $73,394 and a median home value of approximately $280,300, approximately 14% above the national median. Approximately 56,949 renter-occupied households represent approximately 47% of all occupied housing units, and the Saint Paul rental vacancy rate has remained below approximately 5% since 2012, demonstrating structural tightness across all asset classes. Current data points to an average apartment rent of approximately $1,528 per month as of March 23, 2026, up 3.12% year-over-year, one of the stronger rent growth rates among Twin Cities submarkets in 2026. Approximately 43.5% of Saint Paul residents aged 25 and older hold bachelor's degrees or higher, supporting a well-educated and stable renter base. These fundamentals continue to support consistent demand for Minnesota apartment loans across Saint Paul's neighborhoods.

Saint Paul Minnesota Apartment Loan Rates and Financing in 2026

Financing conditions for Minnesota apartment loans remain active in Saint Paul in 2026, with lenders supporting stabilized assets across the city's predominantly Class C and workforce inventory, value-add acquisitions in the pre-war and mid-century rental stock, and newer Class A developments in the Highland Park and Grand Avenue corridors. Approximately 90% of Saint Paul's rental buildings are Class C, containing approximately 77% of all units, with vacancy rates in these buildings at approximately 3%, reflecting exceptional absorption in the city's workforce rental segment. The median property value of approximately $280,300 and a home-value-to-income ratio of approximately 3.8x reflects a moderate affordability profile that channels consistent household demand into the rental market. For borrowers seeking an apartment building loan in Saint Paul, the city's structural vacancy tightness below 5% since 2012, strong workforce rental absorption, and proximity to Minneapolis' major corporate employment corridor provide a practical and income-focused underwriting profile within the broader Minnesota apartment building financing landscape.

Trends in the Saint Paul Minnesota Apartment Market

Saint Paul's rental market benefits from three durable employment pillars: healthcare and social assistance at approximately 26,511 workers, the largest sector, anchored by HealthEast Care System, Regions Hospital, and a network of clinics and specialty providers; manufacturing at approximately 19,793 workers, reflecting the city's legacy industrial base along the Mississippi River corridor; and educational services at approximately 19,338 workers, anchored by the University of St. Thomas, which awarded approximately 3,066 degrees in 2021, Metropolitan State University with approximately 2,187 degrees, and Concordia University-Saint Paul with approximately 2,080 degrees. State government employment anchors the capital district. Saint Paul is one of the most diverse major cities in Minnesota, with approximately 18.1% of residents born outside the United States, and a population that is approximately 17.9% Asian, reflecting a significant and stable Hmong community. Renters in the 25 to 34 age group make up the largest renter cohort at 32%. These fundamentals continue to attract Minnesota apartment lenders evaluating the state's capital market.

Saint Paul Minnesota Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Saint Paul is approximately $1,528 per month, up 3.12% from $1,481 the prior year, one of the stronger year-over-year growth rates among Twin Cities submarkets. The median rent is approximately $1,369 per month, approximately 28% below the national average and approximately 10% below Minneapolis on a comparable basis, reflecting Saint Paul's relative affordability within the metro. By unit type: studios average approximately $1,182/month, one-bedrooms average approximately $1,396/month, two-bedrooms average approximately $1,759/month, and three-bedrooms average approximately $2,508/month. Approximately 51% of all Saint Paul rentals are priced between $1,001 and $1,500 per month, reflecting the predominantly workforce and mid-tier rental base. The Snelling Hamline neighborhood commands the highest rents at approximately $3,084/month for one-bedrooms, and the Macalester-Groveland submarket averages approximately $1,903/month. These rent levels support consistent underwriting for apartment loans in Minnesota where government and healthcare employment anchor stable occupancy.

Saint Paul Minnesota Apartment Loan Supply and Demand in 2026

Saint Paul operates with one of the most durably tight rental supply profiles in the Twin Cities metro. The rental vacancy rate has remained below approximately 5% continuously since 2012, and Class C properties, which represent approximately 90% of all buildings, maintain vacancy rates of approximately 3%, reflecting exceptional workforce rental absorption. Downtown Saint Paul occupancy was projected at approximately 91.8% for Q4 2025, slightly lagging suburban averages, while the Highland-Macalester-Groveland-Summit Hill submarket projects approximately 95.3% occupancy, among the strongest in the entire Twin Cities metro. Approximately 28% of Saint Paul's rental stock was built before 1939, and approximately 59% was built before 1970, reflecting one of the oldest urban rental inventories in Minnesota and a deep pipeline of value-add repositioning candidates. For borrowers pursuing apartment building financing in Minnesota, Saint Paul's structural sub-5% vacancy, strong workforce demand, and high-occupancy neighborhood submarkets support a stable and income-focused underwriting environment.

Opportunities for Apartment Investment in Saint Paul Minnesota

Investors pursuing a Minnesota apartment loan in Saint Paul in 2026 are focused on stable long-term income from workforce housing assets near major government, healthcare, and university employment corridors; value-add acquisitions in the city's large pre-war and mid-century rental stock where a 3% Class C vacancy rate supports pricing power even on dated assets; and stabilized holds in high-occupancy neighborhood submarkets such as Macalester-Groveland and Summit Hill where tenant retention and renewal rates are among the strongest in the metro. Saint Paul's rent growth of approximately 3.12% year-over-year as of March 2026 outpaced Minneapolis and the broader metro, signaling improving fundamentals for capital allocated to the capital city. For Minnesota apartment lenders evaluating the Twin Cities' secondary market, Saint Paul offers structural vacancy tightness dating to 2012, a highly stable government and institutional renter base, and consistent income performance that supports long-term performance for apartment building loans throughout the metro.

2026 Rochester Minnesota Apartment Loan Market Overview

Rochester is Minnesota's third-largest city and the most healthcare-concentrated apartment market in the state for apartment loans in Minnesota, anchored by the Mayo Clinic and the Destination Medical Center initiative, the largest public-private economic development project in Minnesota's history. The city has a population of approximately 122,509 residents as of 2026 with a median household income of approximately $89,389, approximately 17% above the national median and among the highest of any Minnesota city. The median home value is approximately $287,500 and the median monthly rent is approximately $1,316, approximately 13% above the national average. Approximately 17,356 renter-occupied households represent approximately 35% of all occupied housing units. Current data points to an average apartment rent of approximately $1,648 per month as of March 23, 2026, up 3.21% year-over-year, and a median rent of approximately $1,600 as of April 2026, up approximately 6% year-over-year. Rochester was named one of only two Minnesota cities on the 2026 national livability rankings and operates at approximately 2% unemployment, effectively full employment. These fundamentals support consistent demand for Minnesota apartment loans in what is the most Mayo Clinic-dependent and fastest-appreciating secondary market in the state.

Rochester Minnesota Apartment Loan Rates and Financing in 2026

Financing conditions for Minnesota apartment loans remain favorable in Rochester in 2026, with lenders supporting stabilized assets near the Mayo Clinic campus and DMC district, newer Class A inventory anchored by healthcare worker and medical traveler demand, and value-add acquisitions in the city's established 1970s through 1990s rental stock. The median property value of approximately $287,500 is approximately 17% above the national median, and Rochester's vacancy rate of approximately 2 to 3% for apartments is among the tightest secondary market readings in Minnesota. The city's cost of living is approximately 4.7% below the national average despite above-average incomes, creating a fundamentally favorable affordability ratio. For borrowers seeking an apartment building loan in Rochester, the market's effectively full employment, near-zero vacancy in the active rental submarket, and the $5 billion Mayo Clinic Bold Forward Unbound expansion underway provide the strongest single-employer underwriting anchor of any market in the broader Minnesota apartment building financing landscape.

Trends in the Rochester Minnesota Apartment Market

Rochester's rental market is almost entirely driven by the Mayo Clinic ecosystem. The Destination Medical Center initiative, a 20-year, $5.6 billion economic development program, has catalyzed more than $1.6 billion in total private investment since launching in 2013, including more than $1 billion from Mayo Clinic alone. In 2025, Mayo Clinic began preparations for the Bold Forward Unbound expansion, a projected $5 billion investment representing the largest investment in Mayo's 160-year history. The city recorded more than $348 million in new private DMC-district investment in 2025. The population grew approximately 41% from 2000 to 2020, from 85,806 to 121,395, making Rochester one of the fastest-growing mid-sized cities in the Midwest over that period. Olmsted County is projected to grow by approximately 27,400 persons through 2030. Approximately 50.1% of Rochester residents hold bachelor's degrees or higher and renters in the 25 to 34 age group make up the largest cohort at 31%, followed by 15 to 24 year olds at 18%, reflecting the significant medical student, resident, and young healthcare professional renter base. These fundamentals continue to attract Minnesota apartment lenders evaluating the state's most institutionally anchored secondary market.

Rochester Minnesota Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Rochester is approximately $1,648 per month, up 3.21% from $1,597 the prior year, and the median rent is approximately $1,600 per month as of April 2026, up approximately 6% year-over-year, one of the strongest year-over-year rent growth rates in Minnesota. By unit type: studios average approximately $1,223/month, one-bedrooms average approximately $1,493/month, two-bedrooms average approximately $1,727/month, and three-bedrooms average approximately $2,003/month. Approximately 43% of all Rochester rentals are priced between $1,501 and $2,000 per month. The Mayo Run neighborhood commands the highest rents at approximately $1,995/month for one-bedrooms, and Downtown Rochester averages approximately $1,722/month. Rochester rent growth of approximately 3.9% year-over-year as of mid-2025 outpaced the Twin Cities metro and most Minnesota secondary markets, reflecting the structural demand advantage created by apartment loans in Minnesota's most employment-concentrated secondary city.

Rochester Minnesota Apartment Loan Supply and Demand in 2026

Rochester operates in one of the tightest rental supply environments among Minnesota's secondary markets. The city's vacancy rate hovers at approximately 2 to 3%, and the active submarket fills units almost immediately when they become available, with very little new affordable or workforce-level inventory being added. Approximately 22% of Rochester's rental stock was built between 2010 and 2019, the highest new-construction share of any Minnesota secondary market and a reflection of the DMC initiative's decade-long investment cycle, while approximately 15% each was built in the 1970s and 2000s. Two-bedroom units make up the largest share of rental inventory at approximately 41% of all units. A sharp anticipated decline in new deliveries beginning in Q2 2026 is expected to tighten vacancy further, giving well-maintained existing inventory a pronounced competitive advantage. For borrowers pursuing apartment building financing in Minnesota, Rochester's effectively zero vacancy, a $5 billion institutional expansion underway, and no meaningful new supply pipeline provide the most compelling near-term supply-demand profile in the state.

Opportunities for Apartment Investment in Rochester Minnesota

Investors pursuing a Minnesota apartment loan in Rochester in 2026 are focused on stable income-producing properties near the Mayo Clinic campus and the DMC district, long-term holds anchored by the city's structurally replenishing medical professional and patient-family renter base, and value-add acquisitions in the 1970s through 1990s vintage stock where tight vacancy and 3 to 6% annual rent growth support above-average repositioning returns. The city's average commute of approximately 17 minutes, the shortest of any major Minnesota city, reinforces compact quality-of-life appeal for medical professionals who prioritize proximity to the campus. The Bold Forward Unbound expansion will add thousands of new jobs and medical professionals to Rochester over the coming decade, providing extraordinary long-term demand visibility for apartment building loans in the market. For Minnesota apartment lenders evaluating the state's most institutionally anchored secondary opportunity, Rochester offers effectively full employment, a $5 billion single-employer expansion, and near-zero vacancy that supports exceptional long-term performance throughout the metro.

Why Choose Select Commercial for Apartment Loans

What sets Select Commercial apart from traditional lenders and large banks? In this short video, we highlight the key reasons apartment building investors choose to work with us for Minnesota apartment loans between $1.5 million and $6 million. We also actively finance multifamily loans exceeding $6 million.

Here's what the video touches on:

- No upfront application or processing fees

- Fast written pre-approvals often within 24 hours

- Access to a wide range of apartment lenders, not just one bank

- Loan structures tailored to your property and investment goals

Apartment Property Types We Finance in Minnesota

At Select Commercial, we arrange financing for a wide range of Minnesota apartment buildings, from smaller 5+ unit walkups to large portfolios of rental properties. Whether your property is urban, suburban, or mixed-use, we can help you secure the right loan structure based on your investment goals.

- Urban mid-rise and high-rise apartment buildings

- Suburban garden-style apartment complexes

- Small apartment buildings with 5+ units

- Mixed-use properties with residential and limited commercial space

- Underlying co-op apartment building loans

- Portfolios of small apartment or single-family rental properties

- Stabilized buildings with strong cash flow and rent history

If you're not sure whether your property qualifies, contact us for a free quote and we'll review your deal and let you know within 24 hours.

Recent Apartment Loan Closings

Why Minnesota Borrowers Choose Select Commercial

Thousands of apartment building investors trust Select Commercial for our direct, transparent approach and proven expertise in the Minnesota apartment loan market. We're not just brokers, we provide personalized service, fast answers, and access to top institutional lenders without the bureaucracy of traditional banks.

- Over 30 years of apartment loan experience with a national platform

- No upfront fees and fast pre-approvals, often within 24 hours

- Direct access to top lenders offering aggressive terms

- Dedicated support from quote to closing

Want to see why so many clients return to us for their next deal? Start with a free quote – we'll review your scenario and respond quickly.

Our Reviews

Latest Expert Insights from Stephen A. Sobin

Stephen A. Sobin, the president of Select Commercial Funding LLC, is a renowned expert in the field of multifamily financing. His insights and perspectives are regularly sought by leading industry publications. Here are his latest contributions that highlight his deep understanding of the multifamily financing landscape and his commitment to providing clear, insightful analysis on key industry issues.

Navigating Opportunity, Risk as 2025 Winds Down

In an article for Commercial Property Executive titled "Navigating Opportunity, Risk as 2025 Winds Down", Sobin explains as we head into the final stretch of 2025, the commercial real estate industry stands at a pivotal moment. After several years of upheaval—from pandemic disruptions to aggressive Federal Reserve rate hikes and lasting shifts in how people live and work—the sector is entering a new phase.

Why Lower Rates Haven't Fixed Commercial Real Estate

In an article for Wealth Management titled "Why Lower Rates Haven't Fixed Commercial Real Estate", Sobin explains that even as the Federal Reserve has begun cutting rates and borrowing costs should be falling, the commercial real estate sector remains locked in a frustrating stalemate. For high-net-worth investors trying to time the market, he emphasizes that understanding this disconnect requires looking beyond the headlines.

Why the Fed Rate Cut’s a Game Changer for CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that after months of speculation and market anticipation, the Federal Reserve finally pulled the trigger last week, cutting the federal funds rate by 25 basis points to 4.00 to 4.25 percent. read the full article.

Inflation's Current Impact on Apartment

In an article featured in Multi-Housing News, Sobin explains how commercial mortgage rates continue to challenge investors, with elevated inflation depressing real estate market activity. Read the full article.

Will the July Jobs Report Pressure the Fed to Act?

Sobin noted in Multi-Housing News that unemployment hit a three-year high and job creation slowed significantly, factors that could push the Fed to reconsider future rate hikes. Read the full article.

Persistent Inflation and Its Effects on CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that while inflation is still a challenge for the Federal Reserve, there are many positive signs for the commercial real estate industry. The headline Consumer Price Index rose 3.2 percent for the year ended Feb. 29, a figure 20 basis points lower than the Dec. 31, 2023, rate. read the full article.

Commercial Spotlight: Mid-Atlantic Region In this four-state powerhouse, smaller metros are thriving.

In a feature in Scotsman Guide, the Mid-Atlantic Region's real estate dynamics are explored, highlighting its resilience and growth amidst the pandemic.

Stephen Sobin of Select Commercial Funding LLC shared insights on the New York market's allure and the challenges buyers face. He noted the shift from primary urban areas to tertiary markets due to evolving preferences and financial conditions. For a deeper dive into Sobin's analysis, read the full article.

What the New Jobs Report Means for CRE

In an article titled "What the New Jobs Report Means for CRE" in Commercial Property Executive, Stephen Sobin shared his perspective on the latest jobs report and its implications for the Commercial Real Estate (CRE) sector. He highlighted the challenges posed by high interest rates and the prevailing uncertainty in the market. Sobin remarked, "Sellers aren’t selling, buyers aren’t buying... Everyone is waiting because no one knows what to expect." For a detailed analysis and more of Sobin's insights, read the full article.

Decoding "Junk Fees" in Rental Housing

In another latest contribution to Multi-Housing News, Sobin provided expert commentary in an article titled "What's Next for Junk Fees? The Industry Weighs In". He clarified the difference between legitimate fees collected for various third-party services and so-called "junk fees". Sobin emphasized the importance of borrowers understanding their rights in negotiating all loan terms and the obligation of lenders to disclose all fees.

Understanding the Impact of Federal Reserve's Decisions

In a recent article titled "How the Fed's Pause on Interest Rates Impacts Multifamily" published by Multi-Housing News, Sobin shared his expert insights on the Federal Reserve's decision to pause interest rate hikes. He accurately predicted that the Fed would not raise rates in June, citing recent bank failures and lingering concerns about a potential recession.

Stay tuned for more expert insights from Stephen A. Sobin on the evolving multifamily financing landscape.

Frequently Asked Questions About Minnesota Apartment Loans

As of July 5, 2026, Select Commercial offers Minnesota apartment loan rates starting as low as 5.90% on 5, 7, and 10-year fixed-rate options for apartment properties valued between $1.5 million and $6 million. Final rates depend on loan-to-value ratio (LTV), debt service coverage ratio (DSCR), borrower credit and experience, and current market conditions. View the full Minnesota apartment loan rate table above for current pricing across loan terms.

Most lenders require a debt service coverage ratio (DSCR) of at least 1.25, good borrower credit, sufficient net worth and liquidity, and prior real estate ownership experience. Loan-to-value (LTV) ratios typically range from 65% to 80% depending on the loan program and current market conditions. Properties with strong occupancy and clean operating financials qualify for the most favorable Minnesota apartment loan terms.

Most apartment lenders in Minnesota require a 20% to 25% down payment. Your final loan-to-value ratio will be determined by the property's debt service coverage ratio (DSCR), occupancy, location, and overall financial performance.

A qualified broker like Select Commercial can present your loan to many different capital sources, including banks, credit unions, CMBS conduits, agency lenders (Fannie Mae and Freddie Mac), life insurance companies, and private funds. This multi-source approach increases the odds of approval and helps you secure the most favorable rates and terms available across the Minnesota apartment lender market.

The process starts with gathering financials including a current rent roll, trailing 12-month income and expense statement, borrower resume, and a personal financial statement. A mortgage broker will analyze your documents and match you with the best lending program for your Minnesota apartment property. Start with a Free Quote today.

Select Commercial is a leading provider of competitive Minnesota apartment loan rates for properties valued between $1.5 million and $6 million. Through our access to Fannie Mae Small Loan, Freddie Mac SBL, CMBS, life insurance company, bank, and credit union capital, we consistently match borrowers with the lowest available rate and best terms for their specific apartment property. As of July 5, 2026, our Minnesota apartment loan rates start as low as 5.90%.

Yes. While this page focuses on apartment loans under $6 million, Select Commercial also arranges larger balance loans for qualified borrowers. Visit our Minnesota multifamily loan page for options over $6 million.

Agency Small Balance Apartment Loan Programs

Select Commercial connects borrowers with top-tier agency small balance loan programs in addition to bank and private capital options. Featured programs include:

- Fannie Mae® Small Loan Program – For apartment properties with 5+ units and loan sizes from $1 million to $6 million

- Freddie Mac® Small Balance Loan (SBL) Program – Streamlined financing solutions up to $6 million

- Loans Over $6 Million – Explore large-balance apartment loan programs in Minnesota

These agency-backed options offer competitive fixed rates, non-recourse terms, and simplified underwriting for qualified apartment investors.

Minnesota Apartment Building Financing

Select Commercial provides apartment building financing and Minnesota commercial mortgages throughout the state of Minnesota including but not limited to the areas below.