San Francisco Apartment Loans in 2026

At Select Commercial, we specialize in San Francisco apartment loan solutions for local investors, as well as apartment building financing for larger properties and portfolio needs. Our team of experienced apartment lenders is dedicated to offering competitive rates and tailored programs for apartment investments in the area.

If you are looking for apartment loans outside San Francisco but within California, please visit our California Apartment Loan page. For larger properties, we also offer California Multifamily Loans over $6,000,000.

For comprehensive rates on all loan products available across the 48 states, visit our commercial mortgage rates page, where we offer competitive rates for loans starting at $1,500,000. Explore our insights below on the 2025 San Francisco apartment loan market.

| San Francisco Apartment Loan Rates Under $6 Million | Free Loan Quote | ||

|---|---|---|---|

| Loan Type | Rate* | Max LTV | |

| Apartment 5 Yr Fixed | 6.18% | Up to 80% | |

| Apartment 7 Yr Fixed | 6.14% | Up to 80% | |

| Apartment 10 Yr Fixed | 6.28% | Up to 80% | |

Rates shown apply to typical apartment loan requests under $6 million. Investors seeking apartment building financing or an apartment building loan for a purchase or refinance can speak with our apartment lenders for current program details.

Looking for a larger loan? We also offer California multifamily loan programs for properties over $6 million

.San Francisco Apartment Loan Benefits

San Francisco Apartment Loan rates start as low as 5.78% (as of July 31st, 2026)

• A commercial mortgage broker with over 30 years of lending experience

• No upfront application or processing fees

• Simplified application process

• Up to 80% LTV on apartment financing

• Terms and amortizations up to 30 years

• Apartment loans for purchase and refinance, including cash-out

• 24 hour written pre-approvals with no cost and no obligation

Our Reviews

2026 San Francisco Apartment Loan Market: High Barriers to Homeownership Support Rent Growth as the Pipeline Shrinks

San Francisco enters 2026 positioned to benefit from a shrinking delivery pipeline and persistent rent-by-choice demand. For investors comparing apartment building loans, the fundamentals behind a durable San Francisco apartment loan remain the focus: employment trends, the pace of new deliveries, vacancy direction, and rent momentum across the metro.

Employment Losses Ease, But White-Collar Pressure Remains

San Francisco is projected to lose about 0.4% of total jobs in 2026. While this is a smaller decline than the prior three years, continued losses in white-collar roles can outweigh gains elsewhere, making disciplined underwriting important for a San Francisco apartment building loan.

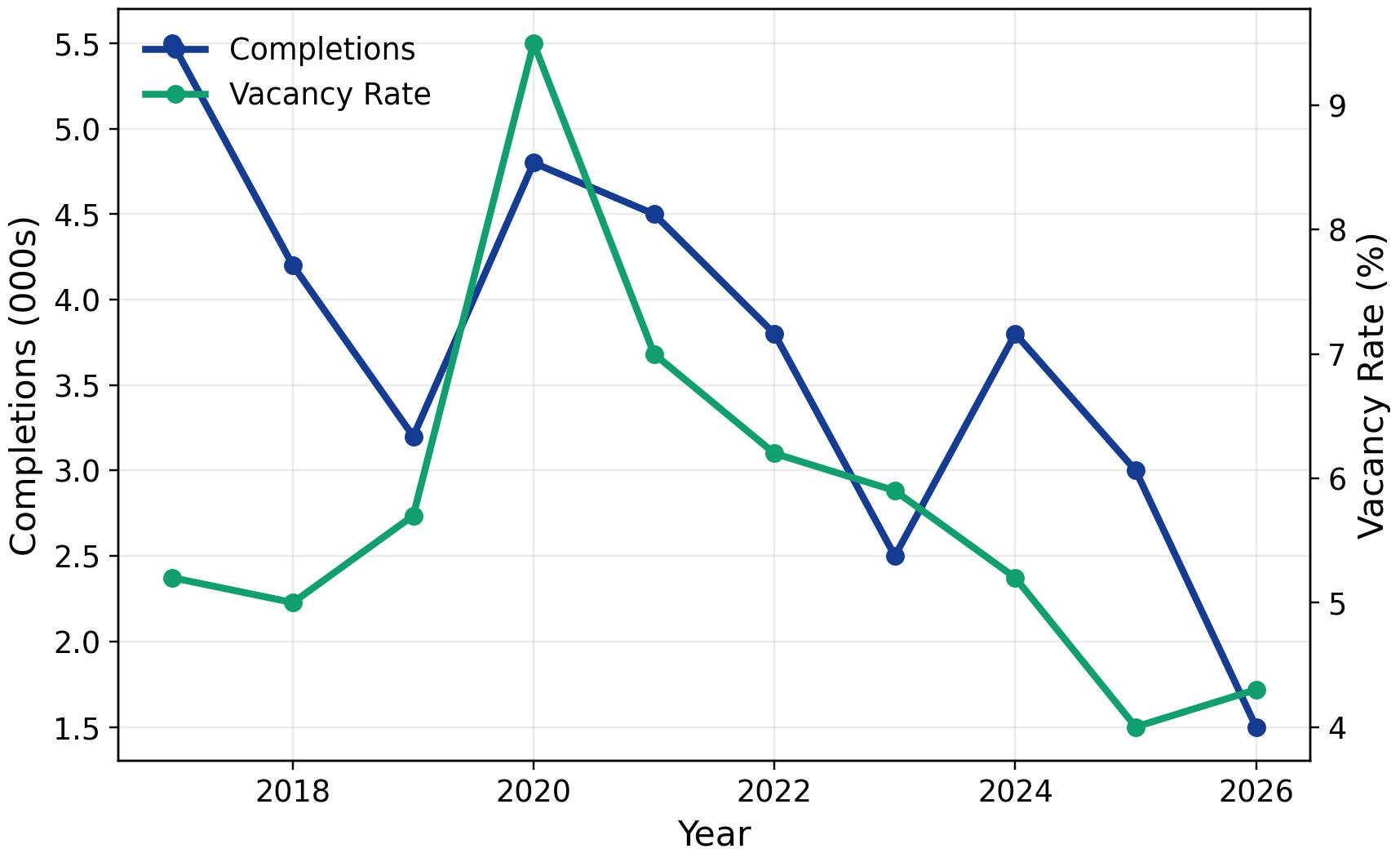

Construction Drops to the Lowest Level Since 2012

The delivery pipeline contracts again in 2026, falling to roughly 1,500 units, the lowest annual level the metro has seen since 2012. A large share of openings is concentrated in San Mateo and Redwood City, which can create submarket variation in lease-up competition for San Francisco apartment loan properties.

Vacancy Ticks Up Slightly After Strong Compression

After a triple-digit basis-point vacancy drop last year, the overall vacancy rate is projected to edge higher by about 30 bps to roughly 4.3% by December. Even with the modest increase, vacancy remains about 70 basis points below the metro's long-term average, supporting a steadier operating backdrop for San Francisco apartment loans.

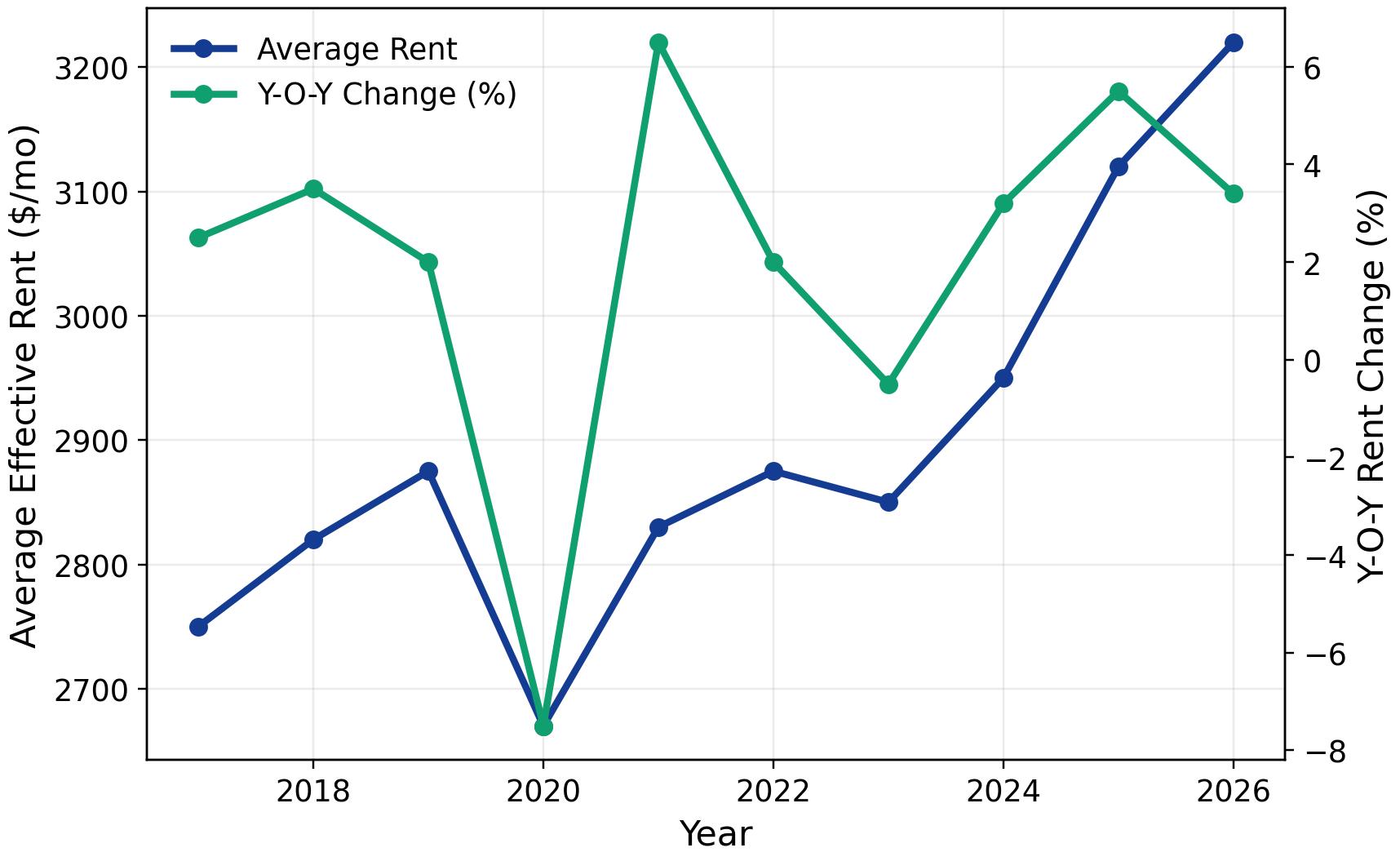

Rent Growth Ranks Among the Strongest Major U.S. Markets

Rents are projected to continue steadily increasing in 2026, with the growth rate ranking among the top five major U.S. markets. Average effective rent is forecast to reach about $3,220 per month by year-end, up roughly 3.4%. For borrowers sizing a San Francisco apartment loan, this supports a more constructive income outlook, especially where demand is strongest.

2026 San Francisco Apartment Loan Market Forecast

- Employment: Total employment projected to decline about -0.4% in 2026.

- Construction: About 1,500 units projected for delivery, the lowest level since 2012.

- Vacancy: Vacancy projected near 4.3%, increasing by roughly 30 bps.

- Rent: Average effective rent projected near $3,220 per month, up about 3.4%.

San Francisco's 2026 outlook is supported by high barriers to homeownership and a shrinking supply pipeline, placing the metro in the top tier nationally for rent growth potential. Demand has been most pronounced in downtown areas, and higher-income renter demand has supported stronger Class A performance metro-wide, even as some nearby submarkets have remained more vacancy challenged.

Transaction activity improved meaningfully last year, signaling a continued flight-to-quality. Multifamily assets built after 2000 have seen stronger sales momentum, and investors may prioritize newer builds to better align with current renter preferences. For borrowers evaluating apartment building loans, a San Francisco apartment building loan strategy in 2026 often comes down to submarket selection, realistic expense assumptions, and rent growth underwriting that reflects the metro's tightening supply backdrop.

Everything You Need to Know About San Francisco Apartment Loan Rates in 2026

In order to determine apartment loan rates in San Francisco, the first thing an apartment building lender needs to know is the type of property involved. Pricing on apartment loans will usually be lower than pricing for certain other commercial property types, as apartments remain a preferred investment in today's market. After the lender understands the asset class, they will look at the deal metrics, which include Loan to Value ratio (LTV), Debt Service Coverage Ratio (DSCR), and Debt Yield. Loans with a lower LTV and higher DSCR are considered less risky and will have better pricing. Another important deciding factor will be the location of the property. Top quality urban and suburban markets will be preferred over rural locations. One other major deciding factor will be the borrower's experience, credit, net worth, and liquidity. Strong borrowers with experience can expect the best pricing. The bottom line is that apartment lenders need to understand the entire picture before quoting rates. As of July 31, 2026, you can check where apartment loan rates currently start, including options for apartment building financing and refinance.

San Francisco apartment loan rates fluctuate based on current market indices. Most apartment loans and apartment building loan programs are priced over one of the following: the US Treasury rate, the Wall Street Journal Prime Rate, or the Secured Overnight Financing Rate (SOFR). In early 2025, all of these rates are still elevated as a result of the Federal Reserve's actions to curb inflation. As market rates gradually soften, apartment loan rates should trend downward. Many borrowers today are not locking in long term fixed rates, but are opting for shorter term structures and lighter prepayment penalties so that they can refinance when rates are more favorable.

It used to be fairly common to obtain 80% financing when rates were in the 3% and 4% range, as the property's cash flow could support higher levels of debt. In early 2025, with many rates in the 6% and 7% range, cash flow is more restricted due to higher debt service costs. We often see maximum loan to value ratios in the 65% to 70% range today as a result of these higher rates. As market rates ease, we would expect to see higher loan to value ratios and lower down payment requirements for apartment building financing.

Lenders look at many items when deciding whether to approve an apartment loan or an apartment building loan. Some of the most important factors include LTV ratio, DSCR ratio, location of the property, property condition, occupancy, and borrower qualifications (experience, credit, net worth, and cash liquidity). While most of these factors are common sense and assumed by borrowers, the DSCR ratio might need some explanation. DSCR stands for Debt Service Coverage Ratio and is a ratio of the total net operating income divided by the annual debt service. Most lenders will require a DSCR of at least 1.25. This means that for every dollar of mortgage payment, the property must net $1.25 in NOI. While the maximum LTV might be 80%, the property still needs to meet the debt service requirements. Due to higher market rates in 2025, many properties will only cash flow at 65% or 70%. It is important to calculate both LTV and DSCR when looking for a new apartment loan.

Latest Expert Insights from Stephen A. Sobin

Stephen A. Sobin, the president of Select Commercial Funding LLC, is a renowned expert in the field of multifamily financing. His insights and perspectives are regularly sought by leading industry publications. Here are his latest contributions that highlight his deep understanding of the multifamily financing landscape and his commitment to providing clear, insightful analysis on key industry issues.

Navigating Opportunity, Risk as 2025 Winds Down

In an article for Commercial Property Executive titled "Navigating Opportunity, Risk as 2025 Winds Down", Sobin explains as we head into the final stretch of 2025, the commercial real estate industry stands at a pivotal moment. After several years of upheaval—from pandemic disruptions to aggressive Federal Reserve rate hikes and lasting shifts in how people live and work—the sector is entering a new phase.

Why Lower Rates Haven't Fixed Commercial Real Estate

In an article for Wealth Management titled "Why Lower Rates Haven't Fixed Commercial Real Estate", Sobin explains that even as the Federal Reserve has begun cutting rates and borrowing costs should be falling, the commercial real estate sector remains locked in a frustrating stalemate. For high-net-worth investors trying to time the market, he emphasizes that understanding this disconnect requires looking beyond the headlines.

Why the Fed Rate Cut’s a Game Changer for CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that after months of speculation and market anticipation, the Federal Reserve finally pulled the trigger last week, cutting the federal funds rate by 25 basis points to 4.00 to 4.25 percent. read the full article.

Inflation's Current Impact on Apartment

In an article featured in Multi-Housing News, Sobin explains how commercial mortgage rates continue to challenge investors, with elevated inflation depressing real estate market activity. Read the full article.

Will the July Jobs Report Pressure the Fed to Act?

Sobin noted in Multi-Housing News that unemployment hit a three-year high and job creation slowed significantly, factors that could push the Fed to reconsider future rate hikes. Read the full article.

Persistent Inflation and Its Effects on CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that while inflation is still a challenge for the Federal Reserve, there are many positive signs for the commercial real estate industry. The headline Consumer Price Index rose 3.2 percent for the year ended Feb. 29, a figure 20 basis points lower than the Dec. 31, 2023, rate. read the full article.

Commercial Spotlight: Mid-Atlantic Region In this four-state powerhouse, smaller metros are thriving.

In a feature in Scotsman Guide, the Mid-Atlantic Region's real estate dynamics are explored, highlighting its resilience and growth amidst the pandemic.

Stephen Sobin of Select Commercial Funding LLC shared insights on the New York market's allure and the challenges buyers face. He noted the shift from primary urban areas to tertiary markets due to evolving preferences and financial conditions. For a deeper dive into Sobin's analysis, read the full article.

What the New Jobs Report Means for CRE

In an article titled "What the New Jobs Report Means for CRE" in Commercial Property Executive, Stephen Sobin shared his perspective on the latest jobs report and its implications for the Commercial Real Estate (CRE) sector. He highlighted the challenges posed by high interest rates and the prevailing uncertainty in the market. Sobin remarked, "Sellers aren’t selling, buyers aren’t buying... Everyone is waiting because no one knows what to expect." For a detailed analysis and more of Sobin's insights, read the full article.

Decoding "Junk Fees" in Rental Housing

In another latest contribution to Multi-Housing News, Sobin provided expert commentary in an article titled "What's Next for Junk Fees? The Industry Weighs In". He clarified the difference between legitimate fees collected for various third-party services and so-called "junk fees". Sobin emphasized the importance of borrowers understanding their rights in negotiating all loan terms and the obligation of lenders to disclose all fees.

Understanding the Impact of Federal Reserve's Decisions

In a recent article titled "How the Fed's Pause on Interest Rates Impacts Multifamily" published by Multi-Housing News, Sobin shared his expert insights on the Federal Reserve's decision to pause interest rate hikes. He accurately predicted that the Fed would not raise rates in June, citing recent bank failures and lingering concerns about a potential recession.

Stay tuned for more expert insights from Stephen A. Sobin on the evolving multifamily financing landscape.

Apartment Loan Types We Serve

If you are looking to purchase or refinance a San Francisco apartment building, don't hesitate to contact us. We arrange financing in San Francisco for the following:

- Large urban high-rise apartment buildings

- Suburban garden apartmentcomplexes

- Small apartment buildings containing 5+ units

- Underlying cooperative apartment building loans

- Portfolios of small apartment properties and/or single-family rental properties

- Other multi-family and mixed-use properties

Apartment Loan Helpful Articles

How to Buy an Apartment BuildingUncomplicated Underwriting

How to Invest in an Apartment Building

Are You Shopping for an Apartment Building Loan?

How To Get The Best Rates On An Apartment Refinance

Recent Apartment Loan Closings

Whether you are purchasing or refinancing, we have the right solutions available for your apartment mortgage loans. We will entertain apartment loan requests of all sizes, beginning at $1,500,000. Get started with a Free Commercial Mortgage Loan Quote.

San Francisco Apartment Loans

Select Commercial provides apartment loans throughout San Francisco, California including, but not limited to, the areas below. We provide apartment loans in most major cities throughout the United States.