North Carolina Apartment Loan Rates

Select Commercial offers some of the most competitive North Carolina apartment loan rates available, with 5, 7, and 10-year fixed-rate options starting as low as 6.10% as of July 20, 2026. As one of the most experienced apartment lenders in North Carolina, we arrange apartment building loans and apartment building financing for properties valued between $1.5 million and $6 million, with up to 80% LTV, 30-year amortizations, and no upfront fees. For loans over $6 million, see our North Carolina multifamily loan options.

| NC Apartment Loan Rates Less Than $6 Million | Free Loan Quote | ||

|---|---|---|---|

| Loan Type | Rate* | LTV | |

| Apartment Loan 5 Yr Fixed | 6.10% | Up to 80% | |

| Apartment Loan 7 Yr Fixed | 6.09% | Up to 80% | |

| Apartment Loan 10 Yr Fixed | 6.09% | Up to 80% | |

| NC Multifamily Loan Rates More Than $6 Million | Free Loan Quote | ||

|---|---|---|---|

| Loan Type | Rate* | LTV | |

| Multifamily Loan 5 Yr Fixed | 5.70% | Up to 75% | |

| Multifamily Loan 7 Yr Fixed | 5.69% | Up to 75% | |

| Multifamily Loan 10 Yr Fixed | 5.69% | Up to 75% | |

*Rates start as low as the rates stated here. Your rate, LTV, and amortization will be determined by underwriting.

North Carolina apartment loan rates are priced based on the U.S. Treasury yield curve. As of July 20, 2026, the 10-year Treasury yield is 4.591% and the 5-year Treasury yield is 4.301%, which directly influences current pricing on apartment building loans in North Carolina.

Want a personalized quote? Click here to request a customized loan quote for your North Carolina apartment property.

Why Select Commercial Offers Competitive North Carolina Apartment Loan Rates

When investors search for the best apartment loan rates in North Carolina, Select Commercial consistently delivers some of the most competitive pricing available for properties under $6 million. We work directly with Fannie Mae Small Loan, Freddie Mac SBL, CMBS conduits, life insurance companies, banks, and credit unions, which means borrowers gain access to a wide network of apartment lenders in North Carolina rather than the rates of a single bank. This multi-source approach allows us to consistently match borrowers with the lowest available rate and best terms for their specific apartment property.

Our North Carolina apartment building financing programs include 5, 7, and 10-year fixed-rate options, up to 80% LTV, 30-year amortizations, non-recourse availability, and no upfront fees. Whether you are acquiring, refinancing, or pulling cash out of a stabilized apartment property valued between $1.5 million and $6 million, our team structures apartment building loans tailored to your investment goals.

Need a multifamily loan over $6 million? Visit our North Carolina multifamily loan page. For other commercial property types, explore our North Carolina commercial mortgage options. To compare all rates nationwide, see commercial mortgage rates.

2026 North Carolina Apartment Loan Market Overview

Entering 2026, North Carolina presents a high-growth apartment market supported by population inflows, job expansion, and business-friendly conditions. For borrowers evaluating apartment loans, the state benefits from strong renter demand across major metros including Charlotte, Raleigh, and Durham. This environment supports apartment building financing strategies focused on absorption, rent growth potential, and long-term demand tied to economic expansion.

Development activity across North Carolina has remained active, with new supply concentrated in high-growth urban corridors. While deliveries have increased, demand continues to keep pace, maintaining balanced vacancy levels. For apartment lenders, North Carolina offers an underwriting profile centered on growth, tenant demand, and forward-looking income performance.

Charlotte Anchors North Carolina Apartment Loans

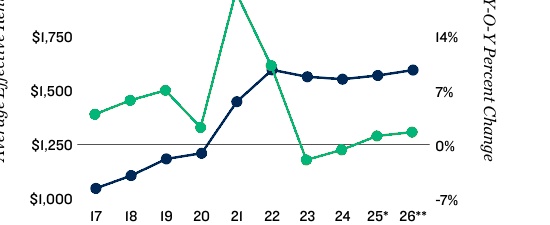

Charlotte remains the primary driver of apartment activity across North Carolina. In 2026, the metro is projected to add approximately 40,000 jobs, deliver roughly 13,000 units, maintain vacancy near 7.0%, and reach average effective rent around $1,600 per month. For borrowers seeking an apartment building loan, Charlotte offers scale, strong population growth, and diversified employment.

Raleigh Reflects Tech and Education Growth

Raleigh provides one of the strongest apartment markets in the Southeast, driven by technology and education. The city has a population of approximately 475,000, median household income near $80,000, median rent around $1,650, and median home value near $420,000. These fundamentals support continued renter demand and rent growth.

Durham Adds Innovation-Driven Demand

Durham complements Raleigh within the Research Triangle, supported by universities and healthcare employment. The city has a population of approximately 290,000, median household income near $70,000, median rent around $1,600, and median home value near $400,000. This supports strong occupancy and long-term demand.

Rent Levels Reflect Strong Growth and Migration

North Carolina continues to show rising rent levels driven by migration and employment growth. Charlotte is projected near $1,600 per month, with Raleigh and Durham slightly higher depending on submarket. This allows borrowers to structure apartment loans across both core and growth-oriented investment strategies.

2026 North Carolina Apartment Loan Market Forecast

- Employment: Charlotte is projected to add approximately 40,000 jobs.

- Construction: Charlotte is projected to deliver roughly 13,000 units.

- Vacancy: Vacancy is projected near 7.0%.

- Rent: Average effective rent is projected near $1,600 per month.

For investors comparing apartment loans in North Carolina, 2026 reflects a market driven by growth and migration. Charlotte provides the primary scale, while Raleigh and Durham offer complementary opportunities tied to technology, education, and healthcare sectors.

2026 Charlotte North Carolina Apartment Loan Market Overview

Charlotte is North Carolina's largest city and the dominant anchor for apartment loans in North Carolina, ranking as the nation's second-largest banking center and one of the fastest-growing major metros in the Southeast, adding approximately 157 residents per day with more than two-thirds between ages 20 and 34. The city has a population of approximately 977,740 residents as of 2026, growing at approximately 1.78% annually, having grown approximately 11.75% since the 2020 census. The median household income is approximately $82,068 and the median property value is approximately $385,700 as of 2024. Approximately 169,668 renter-occupied households represent approximately 48% of all occupied housing units. Current data as of March 23, 2026 shows the average apartment rent at approximately $1,647 per month, down approximately 1.77% from a supply-driven correction, and the median rent at approximately $1,845 per month, approximately 4% below the national average. Construction starts declined approximately 40% year-over-year in 2024, signaling a tightening supply pipeline that is expected to support rent stabilization and recovery through 2026. These dynamics continue to support active demand for North Carolina apartment loans in the state's primary market.

Charlotte North Carolina Apartment Loan Rates and Financing in 2026

Financing conditions for North Carolina apartment loans remain active in Charlotte in 2026, with lenders supporting stabilized assets in proven submarkets, newer construction completing lease-up in the Uptown and South End financial corridors, and value-add acquisitions in the city's large 1990s and 2000s vintage rental stock where elevated recent vacancy has created more attractive entry pricing. The median property value of approximately $385,700 as of 2024 is approximately 44% above the national median, creating meaningful homeownership barriers that structurally anchor the approximately 48% renter-occupied rate among Charlotte's large young professional population. Charlotte's average rent of approximately $1,691 remains approximately 11% below the national average, supporting favorable initial yields relative to comparable Sun Belt metros. For borrowers seeking an apartment building loan in Charlotte, the city's sharply declining construction pipeline, consistent daily in-migration, and nation's second-largest banking center employment base provide a durable underwriting foundation within the broader North Carolina apartment building financing landscape.

Trends in the Charlotte North Carolina Apartment Market

Charlotte's rental market is anchored by the nation's second-largest financial services concentration outside New York City. Finance and insurance leads the employment base at approximately 59,070 workers, anchored by Bank of America's global headquarters, Wells Fargo's East Coast operations hub, Truist Financial, and dozens of major financial institutions that collectively make Charlotte "Wall Street South." Healthcare and social assistance follows at approximately 56,972 workers, and professional, scientific, and technical services at approximately 53,776 workers. The University of North Carolina at Charlotte awarded approximately 8,573 degrees in 2023, the most of any institution in the city, and Central Piedmont Community College approximately 3,208 degrees. The Charlotte-Concord-Gastonia region ranked 11th nationally in numeric population growth, adding approximately 61,000 residents from 2023 to 2024. Approximately 47.4% of Charlotte residents hold bachelor's degrees or higher. The city's median age of approximately 34.5 years and 25 to 44 age group making up approximately 40% of renters reflect a prime young professional demographic. These fundamentals continue to attract North Carolina apartment lenders evaluating the state's primary market.

Charlotte North Carolina Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Charlotte is approximately $1,647 per month, down 1.77% from the prior year's $1,676, reflecting the tail end of a supply-driven correction following record construction deliveries. The median rent across all property types is approximately $1,845 per month, up approximately 2% year-over-year as of April 2026. By unit type: studios average approximately $1,309/month, one-bedrooms average approximately $1,457/month, two-bedrooms average approximately $1,742/month, and three-bedrooms average approximately $2,060/month. Approximately 45% of all Charlotte rentals are priced between $1,001 and $1,500 per month. The South End and Uptown corridors command premium rents well above the city average, while Montclaire South and Windsor Park offer one-bedrooms from approximately $1,045 to $1,080/month. With rent growth projected to reach approximately 4.2% by Q4 2025 as construction slows, Charlotte's rent trajectory supports improving underwriting for apartment loans in North Carolina where young professional in-migration anchors durable absorption.

Charlotte North Carolina Apartment Loan Supply and Demand in 2026

Charlotte is transitioning from a supply-heavy correction toward a more balanced market in 2026. After record apartment completions in 2024 at approximately 16,000 units, and an additional estimated 12,000 units in 2025, the pipeline is sharply contracting with new construction starts down approximately 40% year-over-year in 2024, projecting deliveries of approximately 12,000 units in 2026, well below the record pace. Metro-wide vacancy reached approximately 8.2% at peak in Q3 2025 and is expected to ease toward approximately 6.0 to 6.25% by year-end 2025 and continue normalizing through 2026. Absorption remained solid throughout, with approximately 13,100 units absorbed in the trailing 12 months against 15,527 completions. The most undersupplied outlying submarkets, including Gaston County and Lake Norman, maintained occupancies above 94% with minimal pipelines. For borrowers pursuing apartment building financing in North Carolina, Charlotte's sharply declining construction pipeline, solid in-migration-driven absorption, and normalizing vacancy trajectory support improving near-term underwriting conditions.

Opportunities for Apartment Investment in Charlotte North Carolina

Investors pursuing a North Carolina apartment loan in Charlotte in 2026 are focused on growth and long-term demand from the city's unmatched financial services employment base and daily in-migration, value-add acquisitions in the 1990s and 2000s vintage stock where the recent supply correction has created more favorable entry pricing relative to recent peak-cycle transactions, and suburban stabilized holds in Gaston County, Lake Norman, and the Concord corridor where vacancy near 4 to 6% and minimal new pipelines deliver the strongest near-term occupancy. Charlotte's median household income of approximately $82,068 grew approximately and the Charlotte-Concord-Gastonia metro's addition of approximately 61,000 residents in 2024 provides extraordinary long-term demand visibility. For North Carolina apartment lenders evaluating the state's primary market, Charlotte offers the nation's second-largest financial services concentration, one of the Southeast's most consistent in-migration flows, and a sharply contracting supply pipeline that supports strong long-term performance for apartment building loans throughout the metro.

2026 Raleigh North Carolina Apartment Loan Market Overview

Raleigh is North Carolina's capital and the anchor of the Research Triangle, supporting consistent demand for apartment loans in North Carolina through one of the nation's most concentrated technology, life sciences, and university employment ecosystems. The city has a population of approximately 516,807 residents as of 2026, growing at approximately 1.67% annually, having grown approximately 10.94% since the 2020 census. The median household income is approximately $85,395, approximately 10% above the national median, and the median property value is approximately $418,400 as of 2024, approximately 54% above the national median. Approximately 92,812 renter-occupied households represent approximately 49% of all occupied housing units. Current data as of March 23, 2026 shows the average apartment rent at approximately $1,561 per month and the median rent at approximately $1,735, approximately 11% below the national average, up approximately 2% year-over-year. Raleigh's rental market is recovering from a supply-driven correction with rents showing renewed upward momentum, and the pipeline contracting supports improving conditions for North Carolina apartment loans in the state's tech capital.

Raleigh North Carolina Apartment Loan Rates and Financing in 2026

Financing conditions for North Carolina apartment loans remain active in Raleigh in 2026, with lenders supporting stabilized assets in proven Research Triangle submarkets, value-add acquisitions in the city's large 1980s through 2000s vintage rental stock, and newer construction completing lease-up in the downtown and Midtown corridors. The median property value of approximately $418,400 as of 2024, having more than tripled from $285,400 in 2021, creates significant homeownership barriers that structurally anchor the approximately 49% renter-occupied rate among Raleigh's large young professional population. Raleigh's median rent of approximately $1,468 is approximately 26% above the national average on a gross rent basis, while overall costs remain significantly below comparable tech markets such as Austin, Denver, and Seattle. For borrowers seeking an apartment building loan in Raleigh, the city's technology employment anchors, consistent in-migration, and contracting supply pipeline provide a compelling and improving underwriting foundation within the broader North Carolina apartment building financing landscape.

Trends in the Raleigh North Carolina Apartment Market

Raleigh's rental market is defined by its role as the technology and life sciences hub of the Research Triangle, anchored by three major tech commitments: Apple's $1 billion campus investment creating over 3,000 jobs, Google's $1 billion engineering hub bringing at least 1,000 high-paying positions, and Microsoft's software development center employing approximately 2,500 workers. North Carolina State University, the Research Triangle's largest and most impactful research institution, awarded approximately 10,697 degrees in 2023, the most of any institution in the city, and Wake Technical Community College awarded approximately 5,381 degrees. The broader Raleigh MSA universities collectively awarded approximately 21,032 degrees in 2023, generating exceptional young professional renter demand. Approximately 52.9% of Raleigh residents hold bachelor's degrees or higher, among the highest rates of any Southeast metro. The city's median age of approximately 34.7 years and 25 to 44 age group making up approximately 33.2% of the population reflect a prime technology professional renter demographic. These fundamentals continue to attract North Carolina apartment lenders evaluating the state's technology market.

Raleigh North Carolina Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Raleigh is approximately $1,561 per month, down 1.09% from $1,578 the prior year, reflecting the tail of a supply-correction. The median rent across all property types is approximately $1,735 per month as of April 2026, up approximately 2% year-over-year. By unit type: studios average approximately $1,321/month, one-bedrooms average approximately $1,375/month, two-bedrooms average approximately $1,622/month, and three-bedrooms average approximately $2,002/month. Approximately 53% of all Raleigh rentals are priced between $1,001 and $1,500 per month. The Willmont submarket commands the highest rents at approximately $2,936/month, and the Warehouse District averages approximately $2,113/month for one-bedrooms. Raleigh rents are approximately 14% below the national average for apartment inventory, representing a significant discount to comparable technology metros. These rent levels support consistent underwriting for apartment loans in North Carolina where technology employment growth and NCSU student demand anchor durable absorption.

Raleigh North Carolina Apartment Loan Supply and Demand in 2026

Raleigh's rental market is in the recovery phase of a supply-driven cycle, with the period of softening transitioning into a clear upward rent trend as of early 2026. Recent data shows rents increasing across studios, one-bedroom, and two-bedroom units, with current pricing now exceeding 12-month averages, signaling renewed pricing momentum. The Raleigh market has seen a substantial wave of new construction, but absorption has remained solid throughout, driven by consistent in-migration of technology professionals. New construction starts have declined meaningfully, projecting a tightening pipeline through 2026. Approximately 40% of Raleigh's rental stock was built between 2000 and 2019, reflecting predominantly modern inventory, with the 2010s vintage representing approximately 21% of all units. Two-bedroom units make up the largest share at approximately 42% of all units. For borrowers pursuing apartment building financing in North Carolina, Raleigh's transitioning rent trajectory, contracting supply pipeline, and technology-driven in-migration support improving underwriting conditions through 2026 and beyond.

Opportunities for Apartment Investment in Raleigh North Carolina

Investors pursuing a North Carolina apartment loan in Raleigh in 2026 are focused on growth and high-demand submarkets near Apple, Google, and Microsoft campuses where technology professional incomes averaging approximately $92,178 for 25 to 44 year old households support consistent above-average rent capacity, value-add acquisitions in the 1980s and 1990s vintage stock where supply-cycle pricing adjustments have created more favorable entry costs than the 2022 to 2023 peak, and suburban stabilized holds in the Cary, Apex, and Holly Springs corridors where tech commuter demand and top-rated school systems anchor family renter retention. Raleigh's median household income of approximately $85,395 is approximately 10% above the national median, reflecting the Research Triangle's technology premium on labor incomes. For North Carolina apartment lenders evaluating the state's technology capital, Raleigh offers Apple, Google, and Microsoft campus anchors, NC State University's 10,000-plus annual degree output, and a contracting construction pipeline that supports strong long-term performance for apartment building loans throughout the metro.

2026 Durham North Carolina Apartment Loan Market Overview

Durham is the healthcare, innovation, and university anchor of North Carolina's Research Triangle and a high-demand market for apartment loans in North Carolina, driven by Duke University's global research and medical enterprise, a rapidly growing technology sector, and consistent in-migration of highly educated professionals. The city has a population of approximately 311,965 residents as of 2026, growing at approximately 1.64% annually, having grown approximately 10.75% since the 2020 census. The median household income is approximately $81,619, up approximately 6.06% year-over-year in 2023, and the median property value is approximately $392,800 as of 2024, approximately 45% above the national median. Approximately 57,773 renter-occupied households represent approximately 48% of all occupied housing units. Current data as of March 23, 2026 shows the average apartment rent at approximately $1,533 per month and the median rent at approximately $1,750, up approximately 3% year-over-year. Durham-Chapel Hill saw a remarkable 14.8% jump in median rents from 2024 to 2025, among the top midsize metros nationally, and continued upward momentum is expected in 2026 as limited new construction keeps supply tight. These dynamics continue to support active demand for North Carolina apartment loans in the state's innovation and medical research hub.

Durham North Carolina Apartment Loan Rates and Financing in 2026

Financing conditions for North Carolina apartment loans remain favorable in Durham in 2026, with lenders supporting stabilized assets near Duke University Medical Center, Research Triangle Park, and the downtown innovation corridor, as well as value-add acquisitions in the city's established 1990s and 2000s vintage rental stock. The median property value of approximately $392,800 as of 2024, up approximately 12.2% year-over-year in 2023, creates meaningful homeownership barriers that anchor the approximately 48% renter-occupied rate even among Durham's highly educated professional workforce. Approximately 55.7% of Durham residents hold bachelor's degrees or higher, the highest rate of any major North Carolina city. For borrowers seeking an apartment building loan in Durham, the city's Duke-anchored institutional employment, tight supply constraint relative to Raleigh, and consistent above-average rent growth provide a compelling and differentiated underwriting profile within the broader North Carolina apartment building financing landscape.

Trends in the Durham North Carolina Apartment Market

Durham's rental market is defined by its role as the healthcare and innovation anchor of the Research Triangle. Healthcare and social assistance leads employment at approximately 27,486 workers, dominated by Duke University Health System, one of the nation's premier academic medical centers. Duke University awarded approximately 8,043 degrees in 2023, the most of any institution in the city, generating the largest university renter cohort in the Triangle. North Carolina Central University awarded approximately 1,641 degrees and Durham Technical Community College approximately 1,331 degrees. Total degrees awarded in Durham in 2023 reached approximately 11,160. Durham also hosts major Research Triangle Park employers including IBM, Cisco, and a growing biotech and life sciences cluster. Duke Energy, one of the nation's largest utility companies, is headquartered in Durham. A new children's hospital in nearby Apex is projected to bring approximately 8,000 jobs to the region. Renters in the 25 to 34 age group make up the largest cohort at 34%. These fundamentals continue to attract North Carolina apartment lenders evaluating the state's innovation and medical hub.

Durham North Carolina Apartment Loan Rent Levels in 2026

As of March 23, 2026, the average apartment rent in Durham is approximately $1,533 per month, flat year-over-year, and the median rent across all property types is approximately $1,750, up approximately 3% year-over-year as of February 2026. By unit type: studios average approximately $1,379/month, one-bedrooms average approximately $1,392/month, two-bedrooms average approximately $1,619/month, and three-bedrooms average approximately $1,896/month. Approximately 51% of all Durham rentals are priced between $1,001 and $1,500 per month. Durham rents are approximately 14% below the national average for apartment-specific inventory while remaining approximately 21% above the national average on a median gross rent basis. Durham-Chapel Hill recorded a 14.8% jump in median rents from 2024 to 2025, one of the most aggressive rent growth rates of any midsize metro nationally, creating exceptional value for investors who acquired before this surge. These levels support consistent underwriting for apartment loans in North Carolina where Duke University and biotech sector demand anchors premium rent growth momentum.

Durham North Carolina Apartment Loan Supply and Demand in 2026

Durham operates with a significantly tighter supply profile than Raleigh, a key structural advantage that has contributed to superior rent growth performance. The Durham County rental vacancy rate of approximately 6.3% is within the nationally recognized balanced range of 5 to 10%, while the overall city vacancy of approximately 8.43% reflects broader housing stock including single-family rentals. Durham is described by Research Triangle economists as "smaller and traditionally more constrained when it comes to new construction," meaning pent-up demand is expected to continue benefiting Durham more than its larger neighbor. Approximately 53% of Durham's rental stock was built between 1990 and 2019, with the 2010s vintage representing approximately 19% of all units, reflecting a modern and well-maintained base. Two-bedroom units make up the largest share at approximately 43% of all units. For borrowers pursuing apartment building financing in North Carolina, Durham's supply constraint, superior rent growth trajectory, and Duke-anchored institutional demand support an exceptionally favorable underwriting environment.

Opportunities for Apartment Investment in Durham North Carolina

Investors pursuing a North Carolina apartment loan in Durham in 2026 are focused on long-term growth and income stability from assets near Duke University Medical Center and Research Triangle Park where healthcare and technology incomes averaging approximately $92,000 for prime-age households support above-average rent capacity, value-add acquisitions in the 1990s and 2000s vintage stock where Durham's 14.8% median rent growth from 2024 to 2025 has created significant embedded appreciation relative to entry costs, and stabilized holds in the downtown innovation corridor and American Tobacco Campus area where biotech, startup, and medical professional demand anchors the city's premium submarket. Durham's median household income grew approximately 6.06% year-over-year in 2023 and the city's tighter supply structure relative to Raleigh positions it as the Research Triangle's highest-rent-growth market. For North Carolina apartment lenders evaluating the state's innovation and medical hub, Durham offers Duke University's institutional anchor, superior supply constraint, and one of the highest rent growth rates of any midsize metro, supporting strong long-term performance for apartment building loans throughout the metro.

Why Choose Select Commercial for Apartment Loans

What sets Select Commercial apart from traditional lenders and large banks? In this short video, we highlight the key reasons apartment building investors choose to work with us for North Carolina apartment loans between $1.5 million and $6 million. We also actively finance multifamily loans exceeding $6 million.

Here's what the video touches on:

- No upfront application or processing fees

- Fast written pre-approvals often within 24 hours

- Access to a wide range of apartment lenders, not just one bank

- Loan structures tailored to your property and investment goals

Apartment Property Types We Finance in North Carolina

At Select Commercial, we arrange financing for a wide range of North Carolina apartment buildings, from smaller 5+ unit walkups to large portfolios of rental properties. Whether your property is urban, suburban, or mixed-use, we can help you secure the right loan structure based on your investment goals.

- Urban mid-rise and high-rise apartment buildings

- Suburban garden-style apartment complexes

- Small apartment buildings with 5+ units

- Mixed-use properties with residential and limited commercial space

- Underlying co-op apartment building loans

- Portfolios of small apartment or single-family rental properties

- Stabilized buildings with strong cash flow and rent history

If you're not sure whether your property qualifies, contact us for a free quote and we'll review your deal and let you know within 24 hours.

Recent Apartment Loan Closings

Why North Carolina Borrowers Choose Select Commercial

Thousands of apartment building investors trust Select Commercial for our direct, transparent approach and proven expertise in the North Carolina apartment loan market. We're not just brokers, we provide personalized service, fast answers, and access to top institutional lenders without the bureaucracy of traditional banks.

- Over 30 years of apartment loan experience with a national platform

- No upfront fees and fast pre-approvals, often within 24 hours

- Direct access to top lenders offering aggressive terms

- Dedicated support from quote to closing

Want to see why so many clients return to us for their next deal? Start with a free quote – we'll review your scenario and respond quickly.

Our Reviews

Latest Expert Insights from Stephen A. Sobin

Stephen A. Sobin, the president of Select Commercial Funding LLC, is a renowned expert in the field of multifamily financing. His insights and perspectives are regularly sought by leading industry publications. Here are his latest contributions that highlight his deep understanding of the multifamily financing landscape and his commitment to providing clear, insightful analysis on key industry issues.

Navigating Opportunity, Risk as 2025 Winds Down

In an article for Commercial Property Executive titled "Navigating Opportunity, Risk as 2025 Winds Down", Sobin explains as we head into the final stretch of 2025, the commercial real estate industry stands at a pivotal moment. After several years of upheaval—from pandemic disruptions to aggressive Federal Reserve rate hikes and lasting shifts in how people live and work—the sector is entering a new phase.

Why Lower Rates Haven't Fixed Commercial Real Estate

In an article for Wealth Management titled "Why Lower Rates Haven't Fixed Commercial Real Estate", Sobin explains that even as the Federal Reserve has begun cutting rates and borrowing costs should be falling, the commercial real estate sector remains locked in a frustrating stalemate. For high-net-worth investors trying to time the market, he emphasizes that understanding this disconnect requires looking beyond the headlines.

Why the Fed Rate Cut’s a Game Changer for CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that after months of speculation and market anticipation, the Federal Reserve finally pulled the trigger last week, cutting the federal funds rate by 25 basis points to 4.00 to 4.25 percent. read the full article.

Inflation's Current Impact on Apartment

In an article featured in Multi-Housing News, Sobin explains how commercial mortgage rates continue to challenge investors, with elevated inflation depressing real estate market activity. Read the full article.

Will the July Jobs Report Pressure the Fed to Act?

Sobin noted in Multi-Housing News that unemployment hit a three-year high and job creation slowed significantly, factors that could push the Fed to reconsider future rate hikes. Read the full article.

Persistent Inflation and Its Effects on CRE

In an article featured in Multi-Housing News, Stephen Sobin highlighted that while inflation is still a challenge for the Federal Reserve, there are many positive signs for the commercial real estate industry. The headline Consumer Price Index rose 3.2 percent for the year ended Feb. 29, a figure 20 basis points lower than the Dec. 31, 2023, rate. read the full article.

Commercial Spotlight: Mid-Atlantic Region In this four-state powerhouse, smaller metros are thriving.

In a feature in Scotsman Guide, the Mid-Atlantic Region's real estate dynamics are explored, highlighting its resilience and growth amidst the pandemic.

Stephen Sobin of Select Commercial Funding LLC shared insights on the New York market's allure and the challenges buyers face. He noted the shift from primary urban areas to tertiary markets due to evolving preferences and financial conditions. For a deeper dive into Sobin's analysis, read the full article.

What the New Jobs Report Means for CRE

In an article titled "What the New Jobs Report Means for CRE" in Commercial Property Executive, Stephen Sobin shared his perspective on the latest jobs report and its implications for the Commercial Real Estate (CRE) sector. He highlighted the challenges posed by high interest rates and the prevailing uncertainty in the market. Sobin remarked, "Sellers aren’t selling, buyers aren’t buying... Everyone is waiting because no one knows what to expect." For a detailed analysis and more of Sobin's insights, read the full article.

Decoding "Junk Fees" in Rental Housing

In another latest contribution to Multi-Housing News, Sobin provided expert commentary in an article titled "What's Next for Junk Fees? The Industry Weighs In". He clarified the difference between legitimate fees collected for various third-party services and so-called "junk fees". Sobin emphasized the importance of borrowers understanding their rights in negotiating all loan terms and the obligation of lenders to disclose all fees.

Understanding the Impact of Federal Reserve's Decisions

In a recent article titled "How the Fed's Pause on Interest Rates Impacts Multifamily" published by Multi-Housing News, Sobin shared his expert insights on the Federal Reserve's decision to pause interest rate hikes. He accurately predicted that the Fed would not raise rates in June, citing recent bank failures and lingering concerns about a potential recession.

Stay tuned for more expert insights from Stephen A. Sobin on the evolving multifamily financing landscape.

Frequently Asked Questions About North Carolina Apartment Loans

As of July 20, 2026, Select Commercial offers North Carolina apartment loan rates starting as low as 6.10% on 5, 7, and 10-year fixed-rate options for apartment properties valued between $1.5 million and $6 million. Final rates depend on loan-to-value ratio (LTV), debt service coverage ratio (DSCR), borrower credit and experience, and current market conditions. View the full North Carolina apartment loan rate table above for current pricing across loan terms.

Most lenders require a debt service coverage ratio (DSCR) of at least 1.25, good borrower credit, sufficient net worth and liquidity, and prior real estate ownership experience. Loan-to-value (LTV) ratios typically range from 65% to 80% depending on the loan program and current market conditions. Properties with strong occupancy and clean operating financials qualify for the most favorable North Carolina apartment loan terms.

Most apartment lenders in North Carolina require a 20% to 25% down payment. Your final loan-to-value ratio will be determined by the property's debt service coverage ratio (DSCR), occupancy, location, and overall financial performance.

A qualified broker like Select Commercial can present your loan to many different capital sources, including banks, credit unions, CMBS conduits, agency lenders (Fannie Mae and Freddie Mac), life insurance companies, and private funds. This multi-source approach increases the odds of approval and helps you secure the most favorable rates and terms available across the North Carolina apartment lender market.

The process starts with gathering financials including a current rent roll, trailing 12-month income and expense statement, borrower resume, and a personal financial statement. A mortgage broker will analyze your documents and match you with the best lending program for your North Carolina apartment property. Start with a Free Quote today.

Select Commercial is a leading provider of competitive North Carolina apartment loan rates for properties valued between $1.5 million and $6 million. Through our access to Fannie Mae Small Loan, Freddie Mac SBL, CMBS, life insurance company, bank, and credit union capital, we consistently match borrowers with the lowest available rate and best terms for their specific apartment property. As of July 20, 2026, our North Carolina apartment loan rates start as low as 6.10%.

Yes. While this page focuses on apartment loans under $6 million, Select Commercial also arranges larger balance loans for qualified borrowers. Visit our North Carolina multifamily loan page for options over $6 million.

Agency Small Balance Apartment Loan Programs

Select Commercial connects borrowers with top-tier agency small balance loan programs in addition to bank and private capital options. Featured programs include:

- Fannie Mae® Small Loan Program – For apartment properties with 5+ units and loan sizes from $1 million to $6 million

- Freddie Mac® Small Balance Loan (SBL) Program – Streamlined financing solutions up to $6 million

- Loans Over $6 Million – Explore large-balance apartment loan programs in North Carolina

These agency-backed options offer competitive fixed rates, non-recourse terms, and simplified underwriting for qualified apartment investors.

North Carolina Apartment Building Financing

Select Commercial provides apartment building financing and North Carolina commercial mortgages throughout the state of North Carolina including but not limited to the areas below.