![]() Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

San Diego, California

San Diego Commercial Mortgages in 2026

As a San Diego commercial mortgage broker with 30+ years of experience, Select Commercial finances office, retail, industrial and mixed-use property from $1,500,000, with rates as low as 6.37% and up to 75% LTV. See current rates on every loan type we offer.

Get a Free QuoteFinancing Options in San Diego

San Diego apartment, multifamily and commercial properties each have dedicated financing. Pick the page that matches your property:

Financing more of the state? See California commercial mortgages and California apartment loans.

Financing in another state? Explore our apartment loans, multifamily loans and commercial mortgages nationwide.

San Diego Commercial Mortgage Rates

| Loan Type | Rate* | Max LTV |

|---|---|---|

| Commercial Real Estate | 6.77% | Up to 75% |

| Single-Tenant Net Lease | 6.37% | Up to 75% |

| Owner-Occupied / SBA | 6.57% | Up to 90% |

| Apartment / Multifamily | 5.78% | Up to 80% |

- San Diego commercial mortgage rates as low as 6.37%

- Up to 75% LTV commercial, 90% owner-occupied

- Terms and amortizations up to 30 years

- Purchase and refinance, including cash-out

- No upfront application or processing fees

- 48-hour written pre-approvals, no cost or obligation

Rates last updated August 2026. Rates and maximum LTV shown represent our best-case pricing scenarios. Actual rates, LTV, and loan terms are subject to underwriting approval and may vary.

San Diego Commercial Mortgage Benefits

- San Diego commercial mortgage rates as low as 6.37% on qualifying net-lease property

- A commercial mortgage broker with 30+ years of lending experience

- No upfront application or processing fees

- Up to 75% LTV on commercial property, 90% on owner-occupied with SBA

- Terms and amortizations up to 30 years, purchase and refinance including cash-out

- 48-hour written pre-approvals, no cost and no obligation

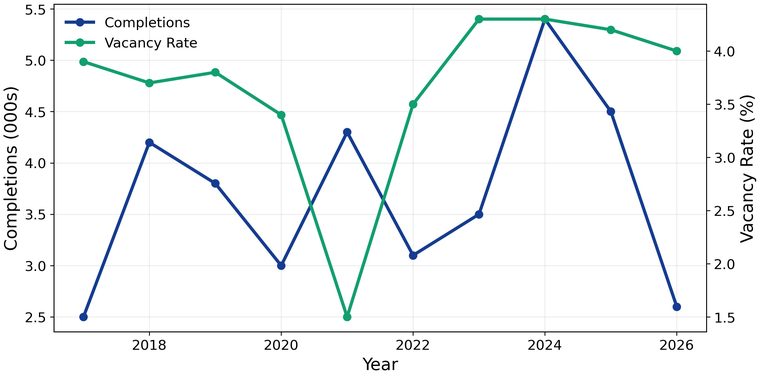

2026 San Diego Commercial Real Estate Market Outlook

San Diego commercial demand tracks the metro’s economy and employment base, the same drivers lenders weigh when underwriting a San Diego commercial mortgage. Office, industrial, retail and mixed-use each move to their own cycle, but a healthy local economy underpins them all.

San Diego Economy and Employment

Hiring improves modestly across San Diego, translating to an additional 6,000 roles, though the traditional office-using sector may continue to record near-term job losses.

San Diego Commercial Supply and Absorption

New commercial construction across office, industrial and retail in San Diego remains below the long-run average, which helps hold vacancy in check for stabilized buildings. A constrained pipeline strengthens the cash-flow story lenders want to see on a San Diego commercial mortgage, and well-located space continues to lease.

San Diego Cap Rates and Investment Activity

San Diego commercial cap rates have largely stabilized after a repricing cycle, and investment activity is picking up as the bid-ask gap narrows. Owner-users remain active with SBA financing up to 90% LTV, while investors focus on stabilized, cash-flowing assets and a growing wave of loan maturities is driving refinance demand.

San Diego Commercial Mortgage Rates and Underwriting

Most San Diego commercial mortgages price over the 5, 7 or 10 year Treasury rather than the Prime Rate. Those benchmarks remain elevated versus the last cycle, so 2026 San Diego deals are sizing to debt-service coverage more than to a headline LTV. Buildings with strong occupancy and a debt-service-coverage ratio of at least 1.25x are clearing underwriting comfortably, and stronger tenants and longer leases earn the best pricing.

San Diego Commercial Property Types

- Industrial: generally the strongest sector, with tight vacancy near transportation corridors.

- Retail: neighborhood and necessity retail is resilient; national credit net-lease tenants price best.

- Office: selective, with premium and medical office financeable and commodity space more conservative.

- Mixed-use and multifamily: the deepest lender pool, supported by steady rental demand.

San Diego Commercial Real Estate Loans We Arrange

Whether you are purchasing or refinancing in San Diego, we arrange financing across every major commercial property type:

San Diego Apartment and Multifamily Loans

Apartment and multifamily lending is a core part of our business. We finance garden apartments, mid-rise and high-rise buildings, student and senior housing, and mixed-use property, with agency, bank, FHA and CMBS options up to 80% LTV. For 5+ unit buildings in San Diego, see our San Diego apartment loans.

San Diego Office Building Loans

We lend on office property in San Diego, both multi-tenant and single-tenant, for investors and owner-users. Investor office typically reaches 75% LTV and owner-occupied up to 90% with SBA, usually fixed for 5, 7 or 10 years on a 25-year amortization.

San Diego Retail and Shopping Center Loans

We finance retail in San Diego from strip centers to single-tenant NNN net-lease stores. National credit tenants earn the best terms; we are more conservative on local, short-lease retail.

San Diego Industrial and Warehouse Loans

Industrial property, warehouse, distribution and flex space, remains a favored asset class in San Diego, often owner-occupied. We look for good locations with access to population centers and transportation.

San Diego Owner-Occupied and SBA Loans

Business owners buying their own San Diego building can reach up to 90% LTV through SBA programs, a strong option for offices, medical practices, and special-purpose property.

San Diego Special-Purpose and Bridge Loans

We also arrange self-storage, hotel, mobile home park and other special-purpose financing, plus short-term bridge loans for San Diego properties in transition or lease-up. Our capital sources include national and regional banks, Fannie Mae, Freddie Mac, FHA and HUD, insurance companies, CMBS conduit lenders, credit unions and private lenders.

Recent Commercial Closings

A sample of commercial and apartment loans we have arranged for investors nationwide.

Other Property & Loan Types We Finance in San Diego

As a full-service commercial mortgage broker, we arrange San Diego financing across every major property and loan type:

We consider commercial loan requests of all sizes, beginning at $1,500,000.

How We Help San Diego Commercial Mortgage Clients

Select Commercial is a leading San Diego commercial mortgage broker. We arrange financing for owners and purchasers of commercial real estate throughout San Diego and the surrounding California area. While we lend across the continental United States, San Diego is a market we actively originate in. With 30+ years of experience, we compare many sources of capital, national banks, regional and local banks, Fannie Mae, Freddie Mac, FHA and HUD, insurance companies, CMBS conduit lenders, credit unions and private lenders, to fit each client. We charge no upfront application or processing fees and typically offer 24-to-48-hour written pre-approvals with no cost and no obligation. Our long-term fixed rates are competitive and we look to close within 45 days of application. For 5+ unit apartment buildings, see our San Diego apartment loans.

What Our Clients Say

“As a real estate attorney, I trust that Select Commercial will deliver commercial mortgages in a timely manner. My clients are always handled professionally, and the rates and terms are excellent. I heartily recommend them.”

David S. · New York City“I needed an SBA loan and found Select Commercial. It was obvious Stephen knew everything about commercial loans. If you are starting a small business, definitely give them a call.”

Larry S. · Washington, DC“Select Commercial was very helpful with my commercial mortgage. I needed to increase cash flow due to maintenance on my property. Stephen went over several options and got me the funds while lowering my payments.”

Gary M. · Portland, OR“Select Commercial offered 100% financing for my medical practice when my bank would have required 20% down. They delivered something my bank could not, and handled everything professionally.”

John C. · Boston, MAGet Your San Diego Commercial Mortgage Quote

No cost, no obligation. Written answers within 48 hours on San Diego commercial loans from $1,500,000.

- No application or processing fees

- Written answers within 48 hours

- For 5+ unit and commercial properties, $1.5M and up