![]() Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

Written & reviewed by Stephen A. Sobin, President of Select Commercial Funding LLC

California

California Commercial Mortgages in 2026

Select Commercial arranges California commercial mortgage financing on office, retail, industrial, mixed-use and owner-occupied property, with rates as low as 6.34%, up to 75% LTV (90% owner-occupied with SBA) and terms to 30 years. Compare today’s commercial mortgage rates.

Get a Free QuoteFinancing Options in California

California apartment, multifamily and commercial properties each have dedicated financing. Pick the page that matches your property:

Financing more of the state? See California apartment loans.

Financing in another state? Explore our apartment loans, multifamily loans and commercial mortgages nationwide.

California Commercial Mortgage Rates

| Loan Type | Rate* | Max LTV |

|---|---|---|

| Commercial Real Estate | 6.74% | Up to 75% |

| Single-Tenant Net Lease | 6.34% | Up to 75% |

| Owner-Occupied / SBA | 6.54% | Up to 90% |

| Apartment / Multifamily | 5.70% | Up to 80% |

- California commercial mortgage rates as low as 6.34%

- Up to 75% LTV commercial, 90% owner-occupied

- Terms and amortizations up to 30 years

- Purchase and refinance, including cash-out

- No upfront application or processing fees

- 48-hour written pre-approvals, no cost or obligation

Rates last updated August 11, 2026. Rates and maximum LTV shown represent our best-case pricing scenarios. Actual rates, LTV, and loan terms are subject to underwriting approval and may vary.

California Commercial Mortgage Benefits

- California commercial mortgage rates as low as 6.34% on qualifying net-lease property

- A commercial mortgage broker with 30+ years of lending experience

- No upfront application or processing fees

- Up to 75% LTV on commercial property, 90% on owner-occupied with SBA

- Terms and amortizations up to 30 years, purchase and refinance including cash-out

- 48-hour written pre-approvals, no cost and no obligation

2026 California Commercial Real Estate Market

Select Commercial arranges commercial mortgages across California, from major metros to smaller markets. Statewide, new commercial construction remains below the long-run average across most property types, which supports occupancy and the cash flow lenders underwrite. Most California commercial mortgages price over the 5, 7 or 10 year Treasury, so 2026 deals size to debt-service coverage, with a debt-service-coverage ratio of at least 1.25x clearing underwriting comfortably.

By property type

- Industrial: generally the strongest sector, tight vacancy near transport corridors.

- Retail: necessity retail is resilient; national net-lease tenants price best.

- Office: selective, premium and medical office financeable.

- Mixed-use and multifamily: the deepest lender pool statewide.

2026 California Commercial Metro Snapshots

The California metros we most actively finance, with 2026 market indicators and the local supply and demand picture:

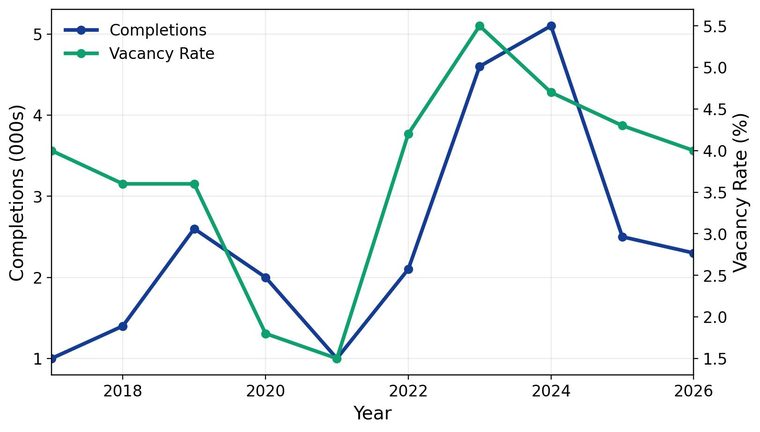

- A limited construction pipeline should keep East Bay vacancy low and support landlords through 2026

- Concord's relative affordability versus inner Bay Area cities should continue to attract renters

- Rent growth is expected to hold in the low single digits as demand stays firm

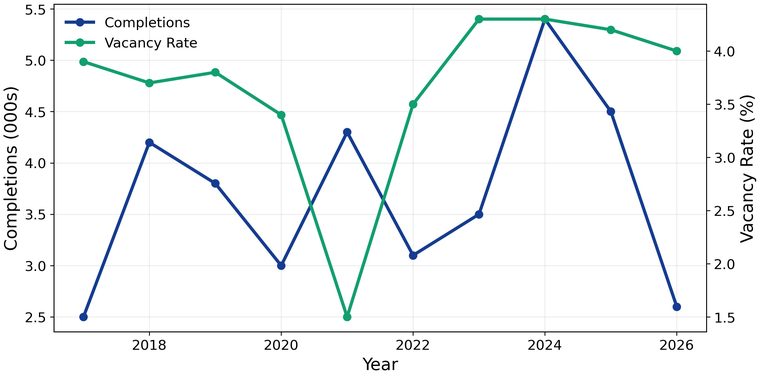

- Limited new construction should keep vacancy low and support steady occupancy

- Rent growth is likely to stay modest as affordability remains a market strength

- Continued job gains in health care and education should sustain rental demand

- Affordability draws LA area commuters

- New projects add to local supply

- Vacancy near 7 percent

- The metro adds 6,000 jobs, a second straight year of modest gains.

- About 6,200 units deliver, the lowest total since 2015.

- Vacancy dips to 4.3 percent, on par with the long-term average.

- Employment: about 6,000 new jobs

- Construction: about 6,200 units, inventory growth below 1% for a fifth year

- Vacancy: around 4.3%, near the long-term average

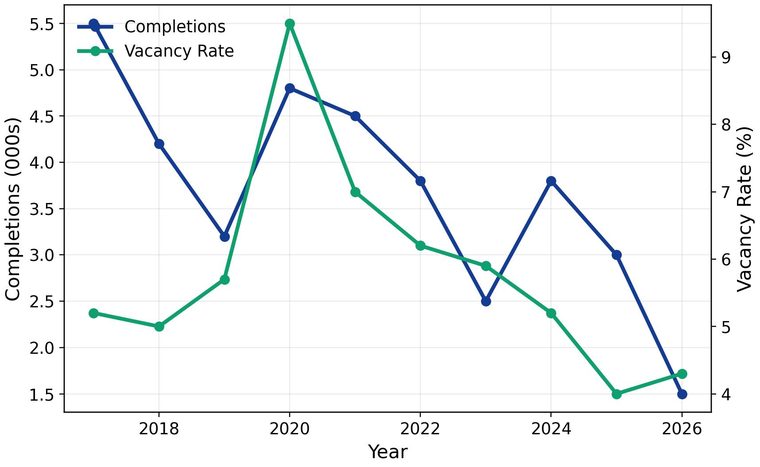

- Job losses ease to the smallest total in four years.

- The delivery pipeline shrinks to its lowest level since 2012.

- Vacancy ticks up to 4.3 percent, still below the long-term average.

- The metro gains 2,500 jobs, its smallest increase since 2020.

- Inventory expands 1.1 percent, matching the prior 10-year average.

- Vacancy falls to 4.0 percent, one of the steepest declines nationally.

- Employment: Net decline of about 3,000 jobs in 2026 (approximately -0.3%).

- Construction: About 1,700 units projected for delivery in 2026.

- Vacancy: Vacancy projected near 4.3%, improving by roughly 10 bps.

- The metro gains 2,500 jobs, its smallest increase since 2020.

- Inventory expands 1.1 percent, matching the prior 10-year average.

- Vacancy falls to 4.0 percent, with the city holding in the 4 percent range.

- Hiring adds 6,000 roles despite office-using sector losses.

- Stock grows 0.7 percent, the smallest annual increase since 2012.

- Vacancy falls to 4.0 percent, among the 15 least vacant major markets.

- Job losses ease to the smallest total in four years.

- The delivery pipeline shrinks to its lowest level since 2012.

- Vacancy ticks up to 4.3 percent, still below the long-term average.

- Employment: About -2,000 jobs projected in 2026 (approximately -0.2%).

- Construction: About 500 units projected for delivery, with inventory growth near 0.3%.

- Vacancy: Vacancy projected near 3.5%, improving by roughly 20 bps.

- Rents stay roughly flat

- Job growth slows notably

- Limited new supply

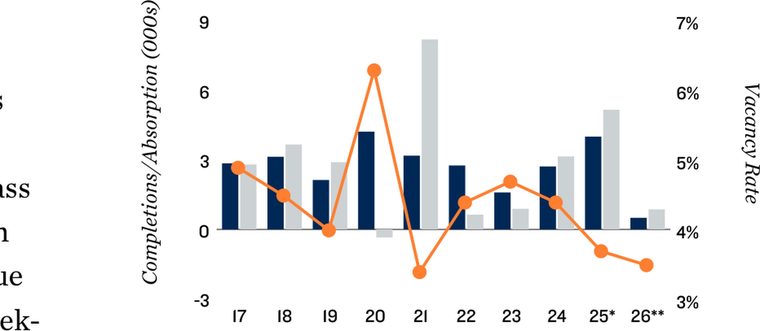

Recent Commercial Closings

A sample of commercial and apartment loans we have arranged for investors nationwide.

Other Property & Loan Types We Finance in California

As a full-service commercial mortgage broker, we arrange California financing across every major property and loan type:

We consider commercial loan requests of all sizes, beginning at $1,500,000.

California Commercial Mortgage Markets We Serve

We provide commercial mortgages throughout California, including:

- Anaheim commercial mortgages

- Bakersfield commercial mortgages

- Chula Vista commercial mortgages

- Concord commercial mortgages

- Corona commercial mortgages

- Costa Mesa commercial mortgages

- El Monte commercial mortgages

- Elk Grove commercial mortgages

- Escondido commercial mortgages

- Fontana commercial mortgages

- Fresno commercial mortgages

- Fullerton commercial mortgages

- Garden Grove commercial mortgages

- Hayward commercial mortgages

- Hollywood commercial mortgages

- Huntington Beach commercial mortgages

- Inglewood commercial mortgages

- Irvine commercial mortgages

- Lancaster commercial mortgages

- Long Beach commercial mortgages

- Los Angeles commercial mortgages

- Modesto commercial mortgages

- Moreno Valley commercial mortgages

- Oakland commercial mortgages

- Oceanside commercial mortgages

- Oxnard commercial mortgages

- Palmdale commercial mortgages

- Pomona commercial mortgages

- Rancho Cucamonga commercial mortgages

- Riverside commercial mortgages

- Sacramento commercial mortgages

- Salinas commercial mortgages

- San Bernardino commercial mortgages

- San Diego commercial mortgages

- San Francisco commercial mortgages

- San Jose commercial mortgages

- Santa Ana commercial mortgages

- Santa Clarita commercial mortgages

- Santa Rosa commercial mortgages

- Simi Valley commercial mortgages

- Stockton commercial mortgages

- Sunnyvale commercial mortgages

- Thousand Oaks commercial mortgages

- Torrance commercial mortgages

- Vallejo commercial mortgages

What Our Clients Say

“As a real estate attorney, I trust that Select Commercial will deliver commercial mortgages in a timely manner. My clients are always handled professionally, and the rates and terms are excellent. I heartily recommend them.”

David S. · New York City“I spoke to several commercial lenders before finding Select Commercial. I was glad I did, because they got me a lower rate and their service was exceptional. If you need a commercial mortgage, you need to talk to Stephen.”

Nathan B. · Philadelphia, PA“Select Commercial was very helpful with my commercial mortgage. I needed to increase cash flow due to maintenance on my property. Stephen went over several options and got me the funds while lowering my payments.”

Gary M. · Portland, OR“I looked elsewhere after two disappointing refinances. I found selectcommercial.com and saw they specialized in commercial building loans. In the end they were by far the best company I have used.”

Jerry T. · Long Island, NYGet Your California Commercial Mortgage Quote

No cost, no obligation. Written answers within 48 hours on California commercial loans from $1,500,000.

- No application or processing fees

- Written answers within 48 hours

- For 5+ unit and commercial properties, $1.5M and up